Better boards, busy bots

by charles | Comments are closed07/29/2026

Making money is art –Andy Warhol

Today’s newsletter is short and mostly sweet. First, helpful hints on building great boards and investment teams, but then some doubts on how much longer it might matter as bot-views and agentic overlords commandeer portfolio management.

Board work matters

A pithy primer on Washington University’s remarkable investment resurgence posted recently on LinkedIn. Clark Hoover, investment officer at the Los Angeles City Employees’ Retirement System read our report on the WashU endowment board’s laudable work and thoughtfully excerpted key dos and don’ts for his nonprofit peers.

When insights come our way – from in-depth interviews with industry veterans, for example – we feel obliged to pass them on to our savvy readers. As ‘frontier’ novelist Louis L’Amour wrote “Knowledge is like money: To be of value it must circulate.”

“What the best boards do:

- Stay aligned and engaged — committed, collaborative, and focused on long-term success.

- Keep governance lean — typically 5–7 members, low turnover, and average board tenure of 10+ years.

- Provide strategic clarity — establish clear objectives, define expectations for the investment team, and evaluate and compensate staff objectively.

- Focus on governance, not management — the board owns strategic asset allocation while empowering investment staff to execute.

What weaker boards tend to do:

- Overcrowd the boardroom — too many voices, high turnover, and excessive micromanagement.

- Send mixed signals — discourage prudent risk-taking while expecting outsized returns.

- Underinvest in talent — reluctance to pay competitively often leads to weaker performance and higher staff turnover.

Strong governance doesn’t guarantee strong investment results—but weak governance makes results much harder to achieve.”

One reader noted, however, that public pensions often have slots set aside for government and union representatives which crowd the boardroom. When it comes to public plans and their financial sway, everyone wants a seat at the table.

Iconoclasts are few and far between and CIOs on many campuses have little room to run, even when they want to. So, if most institutional portfolios look and act the same, why not just give in to AI and the algorithms? It’s cheaper, easier, and when something goes wrong, blame it on those ghosts in the machines.

Sophisticated quant strategies proliferate on Wall Street, ETFs have taken over Main Street, and AI chatbots and robo-advisors swarm financial services. In the world of HR and talent acquisition, algorithms and predictive tools are here in force and impact hiring and career advancement.

Our cyber symbiotes don’t just ease the workload they free us from the tyranny of choice. Decisions without responsibility or regret, every bureaucrat’s dream.

But there are always tradeoffs. Disruptive innovation hits hard and the effects can be brutal. As the automobile swept America, replacing the real life power of horses, entire industries collapsed. Stables, blacksmiths, harness makers, feed suppliers, auction houses, investors; so many livelihoods gone.

So, here’s my worry. These AI dislocations affect perception as well as reality. With deepfakes and synthetic friends, hallucinations and digital shadows, it’s hard to know what part of our digital collective is real.

Financial advisors, analysts, CIOs, all those corporal inhabitants in our world of finance and asset management, in ten years’ time will they still be human? Investing is all about trust and responsibility. AI doesn’t care.

—Charles Skorina

Read More »OCIO Directory Summer 2026: traditional values

by charles | Comments are closed07/04/2026

Customers may forget what you said but they’ll never forget how you made them feel. – Maya Angelou

Our summer 2026 Outsourced Chief Investment Officer (OCIO) directory features one-hundred-eight service providers with contact names, numbers, and emails for each. Our goal is to help families and institutions locate, review, and connect with full-service discretionary outsource investment managers. No ads, no paywall, no charge.

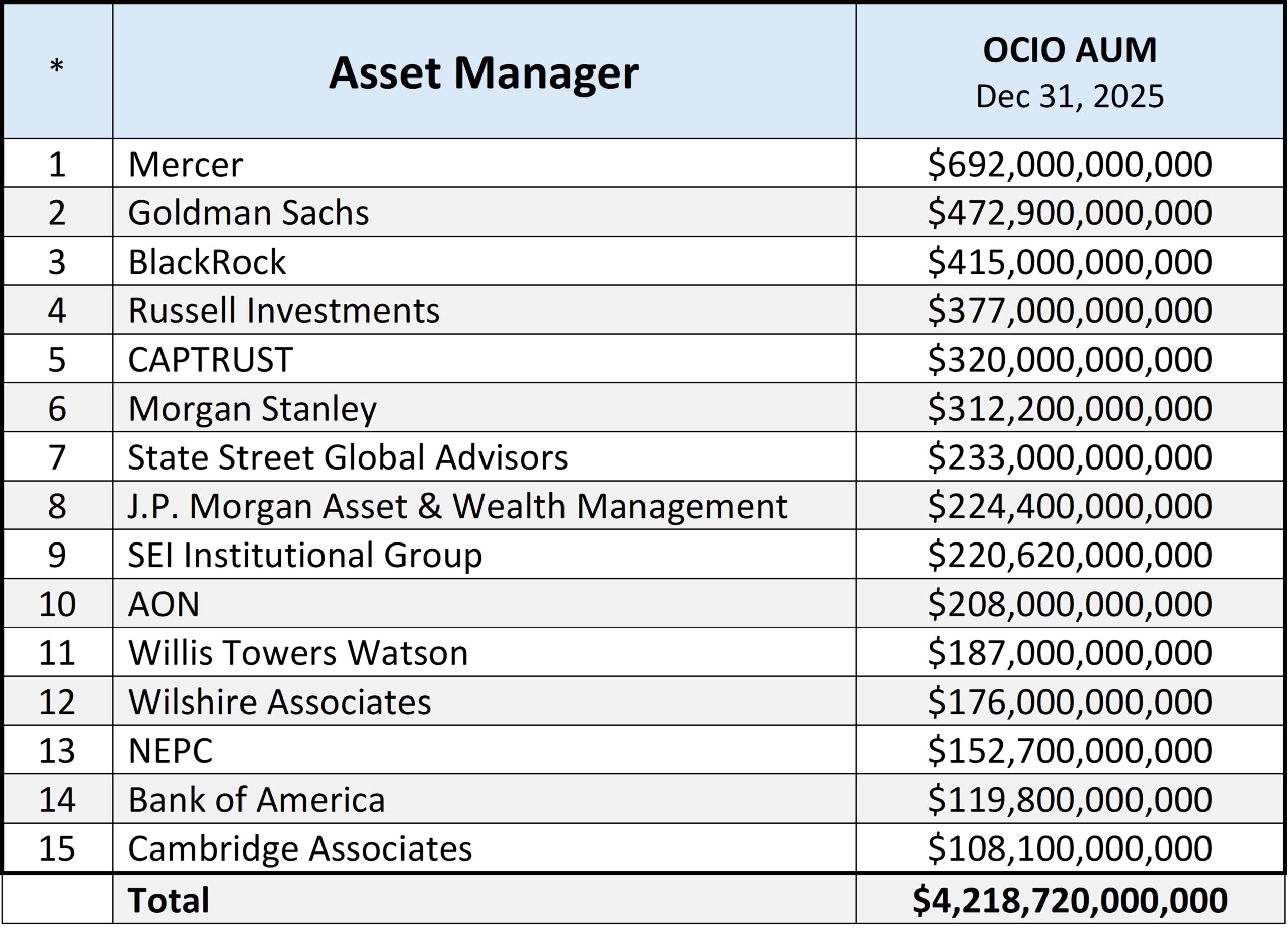

OCIO AUM reached $5.64 trillion at the end of 2025, an 8.9 percent jump ($463bn) from a year ago. And, as usual, the big got bigger. Fifteen firms over one hundred billion manage about seventy-five percent of the assets (mostly pension assets) leaving roughly a trillion four for the pros and pretenders.

{kind=link}

Keeping commitments

The outsourced full-discretion investment business is hyper-competitive, hard to differentiate, and expensive to scale, with hundreds of players including RIAs, banks, brokers, and asset managers all competing for institutional and ultra-high-net-worth discretionary mandates. It’s hard to cut through the clutter.

Worse still, few OCIOs are able to convincingly explain their competitive edge or why it should matter. Most firms read the same on paper. So when it comes down to finals, empathy and likeability usually clinch the deal.

My conclusion after years working with both OCIOs and their clients? Families and nonprofits really don’t care about a firm’s “passion for investing.” They care about service and security and keeping promises, not swaps and overlays and some proprietary secret sauce.

Investment performance may rule one out, but it’s seldom the reason for a winning selection.

The OCIO story is a compelling proposition for many institutions and high-net-worth families, but it’s an intensely competitive arena. If you are not taking care of your client, someone else will.

Stepping up, or stepping out

While some OCIOs up their game, others are moving on. FEG and Hirtle & Co. recently rebranded and reaffirmed their commitments, while Cambridge Associates redoubled its efforts and topped $100 billion full-discretion AUM. Organic growth, not M&A.

Others like Mill Creek, Verus, RockCreek, and Russell (yet again?) have decamped for better-resourced patrons. And, just the other day, Fiducient Advisors, part of Wealthspire, now owned by Madison Dearborn Partners, recently announced plans to acquire Sellwood Investment Partners. M&A every which way.

Without a plan for succession and the resources to compete there’s little choice but to sell or merge.

Speaking of which, we have a client, a regional financial corporation with significant multi-state banking and investment operations, who is seeking to augment their full-discretion, investment management capabilities through acquisitions, mergers, and creative partnerships. In short, we’re looking for a few like-minded OCIOs. Call us if you would like to discuss.

Hirtle & Co., fresh paint, time-honored values

While we’re on the subject of client-centric care, take a look at Hirtle & Co.’s recent rebrand, a firm I’ve known for years. In the firm’s letter to clients managing director Susan McEvoy captures the essence of money and mission:

“What matters more to us is what that capital [client AUM] is multiplying in the world: medical research, education, the arts, and the communities we call home; missions that outlast all of us.”

In founder Jon Hirtle’s words, “I joined Goldman right out of the service (The Marine Corps), with a strong sense of idealism and mission. On my first day in training, I asked my mentor to describe ‘the noble cause.’ He immediately replied, ‘The client.’” That said it all.

Who’s who

If a firm says they provide OCIO services, and their website suggests they do, we’ll usually list them upon request.

However, each OCIO has its own culture, client mix, investment style, and biases. Some firms focus on indexing and liquid markets, others on alternatives, still others on ESG. Some customize portfolios for clients, others don’t. Big, small, specialists, generalists, there’s no lack of choice.

Our advice? When shopping for an OCIO, it pays to be thorough. I recently reviewed investment office performance, operations, and talent with the board of a major university. After numerous interviews with trustees and chief investment officers at peer institutions, my final report included one particular caveat: an OCIO relationship is a marriage not a fling. Once a family or foundation commits to a partner, the bond is not easily undone.

—Charles Skorina

(down PDF newsletter & directory)

Read More »Endowment Performance Rankings 2025: What, me worry?

by charles | Comments are closed01/19/2026

The trend is your friend… until it isn’t. —Anonymous

Our latest endowment performance report features ten-year and one-year returns, along with AUM, for one-hundred-forty-six US and nine Canadian institutions, the latest available.

In our line of work, recruiting talent and creating opportunities for institutional and family office clients, we like hard data on the individuals who manage institutional and family money. Returns may be historical, but they are useful clues to an investor’s views, process, and discipline.

Bulls and brains

For the fiscal year ending June 30, 2025, institutional investors with public equity tilts lived their best lives ever. Chris Hohn et al at TCI, a value orientated, fundamental investor, earned an estimated $18.9 billion in 2025 according to the Wall Street Journal. CNN’s year-end headline said it all. “US stocks just posted a third straight year of stellar gains.”

{kind=link}

*https://www.spglobal.com/spdji/en/commentary/article/us-equities-market-attributes-june-2025/

But it’s never really that simple, is it? Institutional investors operate in an uncertain world and despite the last few years of bull market bliss, the tide inevitably recedes.

As one OCIO industry stalwart writes, the challenge for endowment and foundation investment officers is, “How can we capture real endowment returns that exceed what is required while actively managing downside risk?”

(Exhibit 2, S&P returns since 1950)

{kind=link}

No such thing

When it comes to money, there’s no such thing as passive management. Robert Seawright in We are all active managers contends that “most descriptions of passive investing assume a cap-weighting strategy, but that is necessarily an active choice. Most ETFs use rules-based, non-discretionary approaches, but the rules are all determined by active choice. Moreover, the active/passive performance divide is more about fees than ideology, and fees are chosen.”

Most stakeholders – pensioners, students, faculty, foundation beneficiaries, charity recipients, board members – focus more on today’s headlines and the next budget or grant cycle than what might happen fifty years down the road.

Top institutional investors take a longer view. They temper their emotions, place well researched bets, and hold fast come rain or shine.

Serious matters

Phil Zecher at Michigan State University, for example, our featured chief investment officer in last year’s endowment report, took the helm ten years ago. At that time the endowment ranked forty-two, flat in the middle. Last year MSU’s endowment ranked eighth in our league tables. This year MSU sits at number four. Big moves worth millions. Who says CIOs don’t matter?

Final thoughts

Chief investment officers, investment staffs (and OCIOs) earn serious money for their schools and cost a relative pittance to maintain. Many college athletic programs, on the other hand, are staggeringly expensive as Matt Hayes recounts in USA Today, and their intrinsic contribution to academic health is debatable.

And yet, when coaches meet with college boards the rooms come alive. Excitement builds, time is forgotten, and everyone wants a selfie with these masters of the arena.

But, alas, when CIOs take their turn it’s back to dreary business. Eyelids grow heavy, attention wanders. Like that Philips’ bulb commercial, The Magic’s Gone. Human nature I suppose, but still, endowments pay the bills and keep the lights on.

The U.S. has the greatest university system in the world, a true competitive advantage, thanks to generous donors and visionary leaders, and our endowments are a major source of financial support. Chief investment officers, their staffs and outside managers play a vital role in this success. Let’s show them some love. How about a selfie?

Endowment Performance 2025

We have grouped our endowment performance data into four sections:

122 US endowments over $1bn

23 US endowments, $500mm to $1bn

3 US endowments, non-June 30 FYs

9 Canadian endowments (CAD about $0.70 US)

OCIO firms manage twelve endowments over $1 billion and seven between $500 million and $1 billion among our cohort. They are highlighted in green.

A few public market indexes are included for context.

(Exhibit 3,Various Benchmark Indexes)

{kind=link}

Updates and edits

Try as we might, there are bound to be errors. Please let us know. We will make the changes and send out an update in a few weeks.

To all those who helped us, thank you. We greatly appreciate it.

—Charles Skorina

(download newsletter as PDF) (download tables as PDF)

Read More »OCIO Directory Fall 2025: So many!

by charles | Comments are closed11/19/2025

The price of ability does not depend on merit but on supply and demand. – George Bernard Shaw

For our summer 2023 OCIO directory we wrote: Despite the Nasdaq losing a third of its value, 33%, the Russell 3000 down by 20.48%, the S&P 500 off 20%, and the Dow shedding 9%, total outsourced assets on our list dipped a tenable 9.5%, or $356 billion to $3.4 trillion.

How quickly time flies. Today, with global markets hitting record highs, our latest directory flush with providers, and related AUM over five trillion dollars, discretionary outsourcers of every persuasion are charging ahead chasing assets and fees.

But we can’t help but wonder, are there really that many fully-integrated, conflict-free, financially-grounded, independent investment offices – to paraphrase Hirtle Callaghan’s raison d’etre – fit and able to serve the needs of families, foundations, and related nonprofits?

Supply and demand

There’s torrential demand as waves of new money seek professional advice. And a supply gusher as stalwarts and wannabes rewire their practices for OCIO prospects.

Every week it seems someone we’ve never heard of with three, four hundred million comes calling. Their wealth has surged, they’ve funded a foundation – or sit on the board – and it’s all getting out of hand. Everyone’s after a piece of their pie, they’ve browsed through our directory, and they’re looking for a firm they can trust.

“The US commands an extraordinary 34% of global liquid private wealth and houses 37% of the world’s millionaire population according to the latest Henley & Partners wealth report. And this wealth dominance extends across all brackets, with 36% of the world’s centi-millionaires (those with USD +100 million) and 33% of its billionaires residing in the US.”

Eying the celestial end of the wealth spectrum, the Wall Street Journal reports: “The net worth held by the top 0.1% of households in the U.S. reached $23.3 trillion in the second quarter this year, from $10.7 trillion a decade earlier, according to the Federal Reserve Bank of St. Louis. The amount held by the bottom 50% increased to $4.2 trillion from $900 billion over that period.”

The big squeeze

Pricing plans are crumbling as cost increases and fee compression undercut margins. Revenue on managed assets topped $58 billion in 2024 announced Boston Consulting Group, but almost three-fourths of the gain (70%) came from market performance and a move to lower-priced products.

Meanwhile, it takes a small fortune to field a full-service institutional grade practice as compensation, sourcing, due diligence, cyber-security, audits, and compliance expenses continue to climb.

“Shifts in product offerings and approaches to distribution, industry-wide consolidation, and the need for radically leaner cost structures” are behind the squeeze. To fatten margins, BCG suggests offering actively managed assets such as active ETFs, model portfolios, and separately managed accounts, and offering private assets to retail clients.

But therein lies a dilemma. To truly serve clients, aren’t discretionary outsourcers obliged to avoid the conflicts and temptations endemic in money management? Alicia McElhaney, Institutional Investor, describes the quandary:

“A pioneer in the outsourced chief investment officer business says it’s necessary to be both a pure-play provider — with no products to sell — and have scale. A large asset manager believes disclosing and managing potential conflicts is enough. A search consultant says no OCIO is truly free of competing interests.”

OCIOs everywhere

What exactly is an outsourced chief investment officer? To date there’s no industry standard or designated authority to police the usurpers.

We publish our directory to help families and institutions locate, review, and connect with full-service discretionary outsource investment managers. If a firm says they provide OCIO services, and their website suggests they do, we usually, though not always, add them. But there sure are a lot of them.

[For this issue we removed five firms and added one, Third Lake Partners.]

Institutional grade OCIOs are sophisticated operations. The crème de la crème have years of experience – time to fully hone systems, service, succession, and investment capabilities. Hirtle Callaghan and Blackrock opened for business in 1988, McMorgan & Company set up shop in 1969, Brown Brothers Harriman and JPMorgan Chase date back over two centuries.

Adding to the muddle, each OCIO has its own culture, client mix, investment style, and biases. Some firms focus on indexing and liquid markets, others on alternatives, still others on ESG. Some customize portfolios for clients, others don’t.

Final thoughts

The outsourced full-discretion investment business is hyper-competitive, hard to differentiate, and expensive to scale, with hundreds of players including RIAs, banks, brokers, and asset managers all competing for nonprofit and UHNW discretionary mandates. It’s hard to cut through the clutter.

To quote one industry veteran: “As more and more thoughtful investors recognize the power and promise of OCIO, it’s time to review its three primary requirements.

- A Conflict-Free Structure: OCIO requires a structure that is conflict-free and truly open architecture with no products or hidden corporate agendas to confound decision making.

- Purchasing Power: OCIO requires sufficient purchasing power to pay for talent and support to fully exploit global complexity, noise, and opportunity.

- An Investment Management Culture: OCIOs require a point-accountable, investment management culture.”

Our advice? When looking for an OCIO, it pays to be thorough. Once a family or foundation (or pension fund, healthcare system, insurance company, etc.) commits to a partner, an OCIO relationship is not easily undone.

Charles Skorina

————————————————–

Outsourced Chief Investment Officer

(OCIO) Directory, Fall 2025

Read More »Changing Times

by charles | Comments are closed10/13/2025

“People don’t know what they want until you show it to them.” — Steve Jobs

The late David Swensen, Yale’s formative chief investment officer, found value in dark corners, those unknown managers and overlooked opportunities Heather Gillers referred to in a recent WSJ article. But there hasn’t been much new in money management since Mr. Swensen wrote the playbook.

Whether non-correlated, factor-based, or managed TPA, when we do our ten-year return studies most institutional portfolios look and act the same.

So, here’s a question. If most investment managers think alike, what’s to keep AI and algorithms from taking their jobs?

Barter to Bitcoin

Disruptive technologies and blockbuster products, computers and ETFs, come around maybe once every fifty years, so the time seems ripe for the next big thing — those creative convulsions Professor Clayton Christensen warned about.

Here’s a piece that caught our eye, an excerpt from an article on AI, crypto, and seismic change by Caltech grad and tech founder Ryan W. Sinnet, PhD. A vignette about horses.

In 1920, America reached peak horse: 25 million animals powering the nation’s economy.

But the end had already begun in the cities. In 1910, New York City housed 128,000 working horses, according to the NYC Department of Records. They pulled carriages, delivered milk, hauled freight.

Every morning, thousands of horses trudged through Manhattan streets, their iron shoes striking cobblestones in a rhythm that had echoed through cities for centuries. Smart money owned stables, carriage companies, hay distribution networks. The horse industry wasn’t just big—it was civilization itself. Unthinkable to replace.

Yet by 1920—even as rural America reached peak horse—New York’s horse population had already collapsed to 56,000, more than half gone in a single decade. The transformation was already accelerating.

By 1912, New York City had 38,000 motor vehicles on its streets, and the automobile age had clearly arrived. By 1917, the last horse-drawn trolley made its final trip.

The entire ecosystem that supported horse labor—stables, blacksmiths, harness makers, feed suppliers, auction houses—didn’t evolve or adapt. It vanished. The 25 million horses that powered America in 1920 plummeted to just 3 million by 1960.

Those horses never came back.

Relationships matter

Chatbots, robo-advisors, Zoom, and the cloud are now obligatory parts of the financial landscape. Generations born in the internet age seem fine without the human touch as long as their assets are globally accessible, secure, and earn enough to pay the bills.

But that’s on the retail side. These “digital natives” may be inured to “Tilly Norwoods” and “Schwab Intelligent Portfolios,” but how about foundations, endowments, and UHNW families with large diverse holdings? Might they still want a human at the helm? Someone who “understands their needs and speaks to their sensibilities” as Ken Tsuboi, chief investment officer at McMorgan & Company describes constructive client engagement.

Successful wealth stewards embrace the goals, aspirations, lifestyle preferences, and risk tolerances of their clients. Kathryn George, Partner, Brown Brothers Harriman points out that “Wealth is never just about money. It’s intimately intertwined with relationships – between generations, between values, and between expectations.”

We tallied a record high $4.865 trillion dollars in outsourced assets in our last OCIO report. Rich Nuzum at Franklin Templeton counts the “rise of private market alternatives; the global war for in-house investment talent; the data, digital and technology arms race; and the increasing number of asset owners questioning the need to manage investments in-house” as major factors driving growth.

Funds and families with two billion or more may have the means to field internal investment capabilities, assuming they have the time and patience to build, staff, monitor, and maintain such a business. But for those with less regal sums, outsourcing the complexities and risks to professionals they trust is an effective way to keep their commitments and secure their legacy.

Final thoughts

According to Altrata’s World Ultra Wealth Report 2025 “the total net worth of the UHNW class rose by 6.7% to $59.8tn at the end of June 2025 (and by 11.6% in 2024) – a figure double that of the annual GDP of the US.”

That’s encouraging. After all, managing money is one of America’s key competitive advantages. And we recruit the managers who manage the money.

And yet . . . I can’t help but worry.

“Not because AI does everything better, but because it does enough things cheaply enough that the economics become undeniable” as Dr. Sinnet contends.

About twenty years ago, I had lunch with the EVP of Equities at a major west coast mutual fund company. A fellow University of Chicago grad, he was smart, savvy, and successful, but the lunch ended on a sour note when I remarked that Index funds and ETFs might be a problem down the road for the full-load fund business. Right comment, wrong company.

“I obviously had no idea what I was talking about,” he snapped. “These ETFs are a gimmick with a niche future at best. Clients want the human touch and always will. And they will continue to pay for it.”

Not so long after our lunch he left the firm – retired early I heard – and that giant fund warehouse has had a bumpy ride since.

As Andy Grove, the former CEO of Intel used to say, “only the paranoid survive.” Me? I keep looking over my shoulder.

— Charles Skorina

Read More »{kind=link}