Pay and Performance at Private Foundations

by charles | Comments are closed10/04/2025

What’s worth doing is worth doing for money. — Gordon Gekko (Michael Douglas) Wall Street

What do investment professionals earn at nonprofit institutions? We recruit these executives for a living, so we avidly track their pay and performance.

In this letter we highlight the compensation of one-hundred twenty-eight chief investment officers and staff at private US foundations and tie their pay to five-year performance.

Our goal is to give boards, CEOs, and CIOs a useful set of benchmarks as they consider what to pay their investment executives.

FoundationMark

As always, when it comes to foundation research we draw on the impressive data set from our good friend John Seitz, CEO of FoundationMark.

We think his research and rankings are excellent companions to our pay and performance studies, of interest to asset owners and all purveyors of investment products and services.

The Business of Philanthropy

While college endowments garner most of the media attention, foundations embrace a much larger market, both in numbers and assets.

Over the last thirty years the number of foundations has tripled from about 40,000 in 1995 with assets of $373.4 billion to nearly 120,000 holding $1.6 trillion today. One report puts total nonprofit assets at over $8 trillion dollars.

By comparison, the 2024 NACUBO-Commonfund Study of Endowments lists 658 U.S. colleges and universities and affiliated foundations with $873.7 billion in assets.

Nonprofits are major employers in almost every state. Did you know that:

- The nonprofit workforce is 12.5 million strong, making it the third largest “industry” in the U.S., outdistancing all but two major for-profit industries in its contribution to state employment and payrolls.

- Nonprofit employment is dynamic, growing more rapidly over time than overall employment.

- Nonprofit wages actually exceed for-profit wages in many of the fields where both sectors operate.

(How does foundation pay compare to Wall Street money, you ask? These Heidrick & Struggles comp surveys on alternative asset managers and private equity professionals suggest it’s a toss-up.)

Performance

Unlike academia with its traditions of open access and publish-or-perish, foundations have no impetus to reveal or publish much of anything, particularly investment data, and few do, less than .01%.

As Professors Matteo Binfare and Kyle Zimmerschied found while drafting a paper on foundation investing: “There is little research to date on the investment performance of private foundations.”

Undaunted, Mr. Seitz and staff have developed a system which tracks and estimates the investment performance of most foundations in the nonprofit universe. But please keep in mind that these numbers are estimates based on 990 data, not public pronouncements from the foundations.

Moreover, there’s a long lag – a year and a half to two years – before compensation data is publicly available. Hence, the comp numbers in our table are mostly as of December 31, 2023, with a handful from March and June 2024.

Pass the gravy

Charity often comes down to semantics.

Large private foundations pay their employees well, and for the most part they provide substantial public benefits. The more foundations earn, the more they give away. That’s how the system is supposed to work.

But there are exceptions. We wrote about one case a while back of too much charity staying at home. And Professors Nathan Born and Adam Looney assert in “How Much Do Tax-exempt Organizations Benefit From Tax Exemption?” (pg.8) that a few nonprofit beneficiaries seem reluctant to share their tax-free bounty.

The OCIO Option

The OCIO industry has grown dramatically over the last forty years for good reason, managing institutional money is expensive. It takes time and resources to build a competitive, institutional-grade investment office, and staff compensation alone can run seventy-five to eighty-five percent of total costs.

The top three foundations in our table, for example, disclose investment staff comp of $13,438,547 for the Hewlett, $12,400,949 for the Ford, and $11,133,746 for the Moore, but that’s only for the highest paid employees. The actual investment office headcount and payroll is often much larger.

OCIOs such as Hirtle Callaghan, Blackrock, Brown Brothers Harriman, McMorgan & Company, Third Lake Partners, et al, have spent decades building their platforms and working with organizations and families with like-minded missions, objectives, and challenges.

These full-discretion investment managers offer the proven performance of in-house investment staffs and the process and structure to cope with operational and regulatory headaches, all at a reasonable price.

For most nonprofits under $1 billion AUM, and for many with more, outsourcing is the better choice.

Pay and Performance at Private Foundations

Highest Paid Investment Staff Members

Read More »Smart money

by charles | Comments are closed08/06/2025

If I disagree with something, I either bet against it, or I keep silent – Amarillo Slim

It’s been a festive fifty years for the alternative investment industry, with private equity the belle of the ball. And as Chuck Prince, former CEO of Citigroup once remarked, “as long as the music is playing, you’ve got to get up and dance.” But no matter how compelling the party, there are usually a few contrarians lingering in the wings.

Ken Frier, CEO of OCIO firm Atlas Capital Advisors, wrote recently that “The signs are clear, the non-profit model, where the energy goes toward selection of alternative investment managers, is bearing less fruit.

That’s the case even for the Yale endowment – their performance beat a simple 90/10 stock/bond index portfolio by 6.2% in 1994 – 2004, by 3.6% in 2004 – 2014 and just 1.2% in 2014 – 2024. And that 1.2% in the past decade is overstated since Yale cannot sell their private holdings at the reported value.”

Maybe so, but with private equity forecast to double from $5.8tn in 2023 to $12.0tn in 2029 and the “barbarians” storming the retail 401(k) ramparts, one can’t help but wonder what the smart money is up to. As Ben Carlson, A wealth of common Sense, quipped, “being a contrarian is easier in hindsight.”

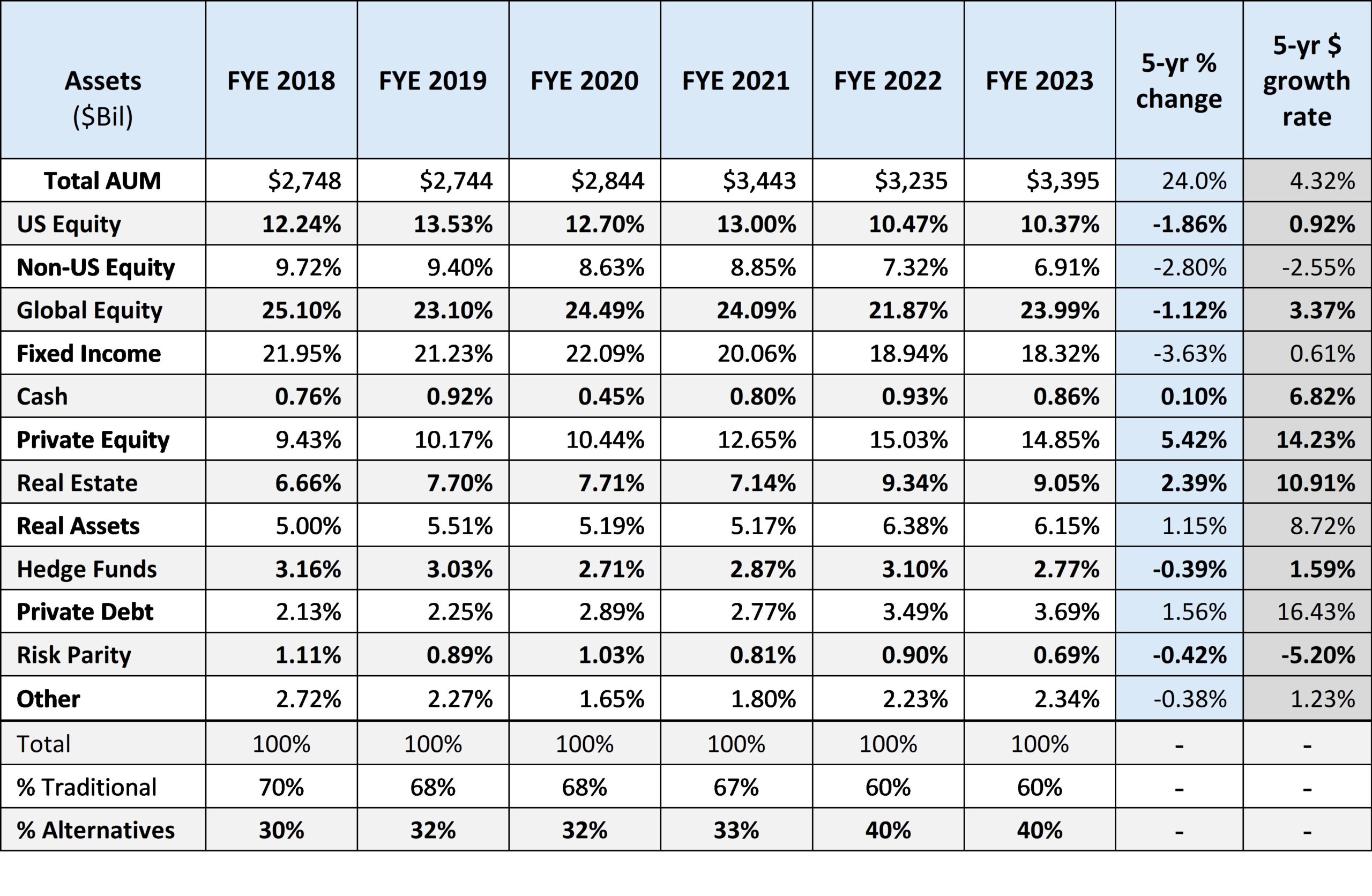

Most big dollar state pensions still follow the herd. CalPERS recently announced they’re going large on private assets with a target 40% allocation, about $225 billion of the $563 billion dollar fund.

As for CalPERS peers, Stephen L. Nesbitt, CEO & CIO of institutional consultant Cliffwater reported last year that allocations to alternatives reached 40% of state pension assets in 2022, with PE at 14.85% as of 6-30-23.

State Pension Allocations

June 30, 2018 to June 30, 2023

{kind=link}

Non-profit Investment staffs try their best, but most go to the same conferences, use the same consultants, follow the same trends, and invest with the same managers as their peers. Career risk is too great to “think different” when politicians and media trolls lie in wait for any and every mistake.

Pinching pennies

Despite the grumbling, fees still don’t seem to matter much to the institutional crowd. Richard Ennis, former co-founder of consulting firm EnnisKnupp (now AON), thinks the herd pays too much for too little.

“Alts bring extraordinary costs but ordinary returns – namely, those of the underlying equity and fixed income assets.” Ennis finds big endowments in his study – estimated to hold 65% of assets in alternative investments – fare worse than pensions, which have a 35% exposure.

When compared with a market index that he designed with a specific stock-bond mix to mimic funds’ risk profile, endowments have trailed by 2.4 percentage points annually in the 16 years through June 2024. Over the same period, pensions undershot their benchmark by 1 percentage point a year.”

Callan recently published their 2025 Cost of Doing Business Study – “a comprehensive look at the investment management fees paid by institutional investors.” Here are a few highlights from the press release:

“Total investment management fees averaged 40 basis points (bps) across all asset pools. But this headline figure masked significant variation across investor types:

- Nonprofits continued to pay the most, averaging 57 bps, driven by larger allocations to alternatives.

- Public funds averaged 43 bps, but the largest plans resembled nonprofits in both structure and fees.

- Corporate funds averaged 30 bps, driven by growing use of liability-driven investing (LDI).

- Insurance pools, with their conservative asset allocations, were the lowest at 20 bps.”

To be fair

Read More »OCIO 2025: the winds of change

by charles | Comments are closed07/28/2025

When the winds of change blow, some people build walls and others build windmills ― Chinese proverb

There’s a lot of money to manage in this world, about $471 trillion US dollars according to the latest UBS Global Wealth Report 2025, and well over a third – $175 trillion – sits right here in our own back yard.

Last year Henley Global’s World’s Wealthiest Cities Report 2024 broke down US wealth distribution by individuals and location:

{kind=link}

All this wealth should be good news for investment outsourcers as nonprofits and the nouveau wealthy look to offload their investment headaches. But deep-pocket competition and advances in knowledge-based technologies are changing the game. It’s no time for complacency.

Bots and bolts

Not long after we published our latest OCIO directory, I got a call from the president of a large west coast foundation, unhappy with their OCIO provider’s performance and especially unhappy with the service.

The president explained that they might have stomached the last few years of mediocre returns if communication were timely and forthright, but apparently service was half-hearted and the board had had enough. They are reviewing alternatives.

In the good old days – before TikTok and cat videos – sales, service, and steady returns were the nuts-and-bolts of money management. When Hirtle Callaghan, Commonfund, McMorgan & Company, and Strategic Investment Group hung their shingles the outsourced chief investment officer concept was fresh and intriguing. Still a tough sell, but the field was wide open.

Twenty years ago, when the Princeton Theological Seminary asked me for OCIO referrals I sent the school eight names. Today there are one hundred-eleven firms on our list, and chatbots, robo-advisors, Zoom, and cloud-based access are essential parts of the full-service landscape.

Baby boomers and Gen-Xers still crowd the boardrooms and family seats and most still prefer the human touch, but how and with whom will the next-gens invest?

Digital natives, those born in the internet age – Millennials (1980–1995), Gen Z (1995–2010), and Gen Alpha (2010 – present) – grew up with tech. As long as their assets are globally accessible, secure, and returns pay the bills they don’t seem to care much about human contact.

So, will AI replace human empathy and intuition as Mr. Zuckerberg envisions? Will “Her” soon be our most trusted companion? If so, who or what will manage our money?

Digital shadows

“Most wealth managers say they want more clients. But too often, they wait for them to show up” notes the Boston Consulting Group. But, says BCG, there are powerful tools on the horizon to support business development.

GenAI-powered prospecting engines using external data can identify and profile business owners, expats, and high-income professionals and track digital indicators that suggest investable wealth, such as business sale filings, job changes, bursts of luxury travel reviews, and niche signals like luxury car forums.

“The engine doesn’t just find names, it prioritizes them. An internal scoring system ranks each lead by value and likelihood to convert. High potential prospects can be routed directly to the most suitable advisors, complete with customized outreach packs. Every interaction – open rates, meeting conversions, follow-ups – is tracked and fed back into the model, so it gets smarter over time.”

Noah Smith, in his piece “The dawn of the posthuman age” writes:

“When I was a child, sometimes I felt bored; now I never do. Sometimes I felt lonely; now, if I ever do, it’s not for lack of company. Social media has wiped away those experiences, by putting me in constant contact with the whole vast sea of humanity. I can watch people on YouTube or TikTok, talk to my friends in chat groups or video calls, and argue with strangers on X and Substack. I am constantly swimming in a sea of digitized human presences. We all are.”

Final thoughts

Read More »OCIO directory, spring 2025, Time and Money

by charles | Comments are closed05/22/2025

I never wanted this for you. We just ran out of time, Vito Corleone ― The Godfather

Our spring 2025 Outsourced Chief Investment Officer (OCIO) directory update features one-hundred-eleven service providers with pertinent particulars on each. We include names, numbers, emails, and titles of business executives at each firm ready to take your call.

Our goal is to help families and institutions locate, review, and connect with full-service discretionary outsource investment managers. Our directory makes it easy for prospective clients to reach them. No ads, no paywall, no charge.

Time and Money

Time is a beguiling thing. “The relative progression of existence” posited Einstein. “Mostly a human affair” adds theoretical physicist John Kitching. But for the rest of us, aging is more akin to Hemingway’s famous line, “How did you go bankrupt? Two ways. Gradually, then suddenly.”

Succession, like the passage of time, is something most families and institutions are aware of, but surprisingly few do much about it.

To be fair, sometimes age and events disrupt the best laid plans. A few weeks ago, I met with a notable, highly successful founder and entrepreneur who wished to discuss recruiting a new family office head. Due to this individual’s distinctive longevity, past occupants in the position are no longer with us.

This patriarch is still sharp as a tack and busy juggling ideas and opportunities, but time is short, there’s much to do, and the odds of replacing a time-tested veteran with a like-minded newbie and bringing this fresh hire up to speed in months, not years, are growing longer by the day.

Planning ahead

In the OCIO business it takes years to establish a presence, polish services, and build a solid investment record. Few firms manage the task. Even fewer adapt, revitalize, and deliver across generations.

Recent years have seen a steady stream of outsourcing hopefuls merge with better-resourced patrons as founders age out and cash in. Recent capitulants include Hall Capital, NEPC, Agility, Truvvo, Ellwood Associates, New Providence, CornerStone, PFM, and Permit Capital.

But now and then a firm manages the transition. Hirtle Callaghan, a pioneering OCIO serving philanthropic families and mission-driven nonprofits, opened for business thirty-seven years ago and recently finished fine-tuning their plans for the next fifty years.

Jon Hirtle remains Executive Chairman and works full-time, but the firm has transitioned to a distributed leadership structure with firm-wide support to provide stability and continuity. A three-member management committee now leads the firm, buttressed by ten managing directors and thirty directors.

While controlling interest remains within the Hirtle family – two generations of family members currently in leadership positions – the firm continues to parse out equity and mentor next-gen talent.

There were a few twists and turns along the way, but clients are pleased and the future looks bright.

The sunny side

It turns out, when time flies by, we’re usually having fun. That’s according to a University of Nevada, Las Vegas report.

“We tell time in our own experience by things we do, things that happen to us,” said James Hyman, a UNLV associate professor of psychology and the study’s senior author. “When we’re still and we’re bored, time goes very slowly because we’re not doing anything or nothing is happening.

On the contrary, when a lot of events happen, each one of those activities is advancing our brains forward. And if this is how our brains objectively tell time, then the more that we do and the more that happens to us, the faster time goes.”

In other words, we can choose between a seemingly short but fruitful life, or one long boring slog. Me, I think I’ll fruitfully keep on recruiting.

― Charles Skorina

(download OCIO Directory only as PDF)

Read More »Foundation Investing: if you’ve seen one private foundation…

by charles | Comments are closed04/18/2025

Let me tell you about the very rich. They are different from you and me. ― F. Scott Fitzgerald, The Great Gatsby

Suppose the Princeton or Yale endowment investment staff wanted to go all-in on a single stock? Forget diversification and the free lunches, just one shoot-the-moon can’t lose security. Think their trustees would go for it? Can elephants fly? Of course not.

And yet, this is the case for some of the biggest winners in the foundation world, funds like the Jen-Hsun & Lori Huang Foundation and the Lilly Endowment.

So, here’s a question. Does foundation management mirror the personalities and proclivities of their anomalous founders? And, if so, how have these various styles affected investment performance over the last five years?

For example, a preference for public markets versus alternatives, concentration versus diversification, or sports teams and crypto.

Awash in liquidity

Thanks to several extraordinary decades of wealth creation, (present speed bumps aside) private foundations and their ultra-high-net-worth benefactors are flourishing.

Over the last thirty years the number of foundations has tripled from about 40,000 in 1995 with assets of $373.4 billion to nearly 120,000 holding $1.6 trillion today.

Given a record $19.4 trillion in liquid assets in checking and savings accounts and money market funds, an S&P annual return of 9.33% over the last thirty years, and unabated philanthropic zeal among the 225,000 U.S. ultra-wealthy mega-donors, private foundations – the Getty, Casey Family Programs, the Summer Science Program – continue to play a major role in American life.

Jon Hirtle, executive chairperson of OCIO provider Hirtle Callaghan puts it this way:

Foundations are responsible for a meaningful portion of society’s accumulated and monetized patrimony. That financial patrimony is used to enhance social services, the arts, scholarship, research…human progress, if you will. So, better foundation investing means more human progress. How about that for an inspiring mission?

Ornery, reclusive beasts

Read More »{kind=link}