‘Banner Year’ Doesn’t Mean ‘Money in the Bank’ for Endowments

by charles | Comments are closed12/10/2021

Venture Capital: Marks to Make-Believe

by charles | Comments are closed12/04/2021

Occasionally we publish commentary from other sources. This short piece from PitchBook on venture capital’s skyrocketing valuations is a timely follow up to our last note on investment returns 2021.

As Mary Cahill, former Emory University CIO, commented in a recent Fundfire post, “Gains on paper are not the same as money in the bank.”

Speaking of investment returns, the last two years under Covid have been strange days indeed. Half the population can’t make rent, while the other half – anyone with assets – runs the table.

One year ago, in FY2020, university endowment returns averaged 1.8 percent. This year our back-of-the-envelope calculations suggest an average in the low thirties.

It’s anybody’s guess what next year will bring, but we’ll leave you dear readers with these words of investment wisdom from a master of the craft.

“Go for a business that any idiot can run – because sooner or later any idiot probably is going to be running it.”

― Peter Lynch

Best wishes for the Holidays and a great 2022.

— Charles Skorina

VC-backed IPOs are booming, yet public performance this year is lagging

PitchBook, December 4, 2021

Has 2021’s ramp-up in IPO activity been a rush to the exits prior to a change in the market cycle?

Is it just the new normal?

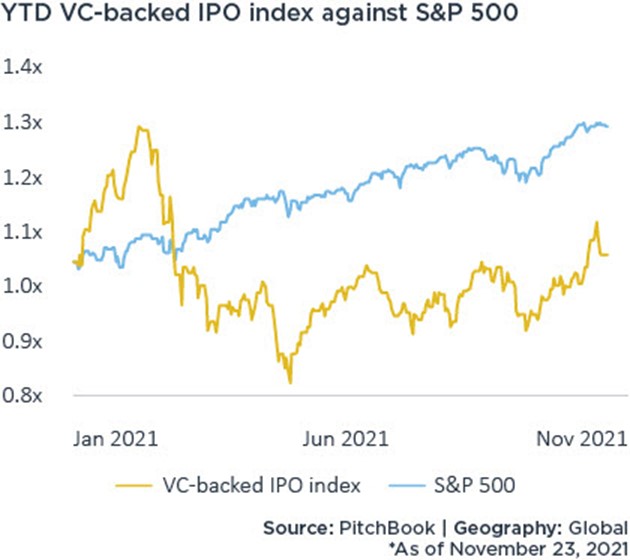

Time will tell, but one thing is certain: US VC-backed IPOs have broken all kinds of records this year, unlocking more than $500 billion of liquid value.

The median company valuation at IPO is nearly 60% greater than its last private valuation. However, our VC IPO index has shown relative underperformance against the S&P 500 since the beginning of 2021.

{kind=link}

Long-term performance still shows above-market returns, but inflationary pressure and the increased expectations of interest rate hikes in the coming year have introduced more volatility in the market for these freshly public companies.

These swings have been especially potent in the software space, which represents nearly 50% of the total weight of the IPO index, as the lofty valuation multiples placed on those companies have received a reality check in the face of rising discount rates.

While the majority of the underperformance came earlier in the year, it remains top of mind given the signs of increased market uncertainty—which have been amplified by fresh pandemic-related concerns.

This represents a significant threat to the sustainability of the IPO volumes we’ve seen over the last couple of years, as negative price performance or just general uncertainty will discourage IPO plans for certain startups, especially if they have access to other financing and liquidity options.

We will maintain vigilant coverage of this space as we expect IPOs and their performance to be a leading indicator on the health of the VC industry, as public markets have facilitated the majority of exit value over the last two years.

For more data and analysis, click to download our free Index of Venture-Backed IPOs.

Feel free to reach out with any feedback or questions, or if you would like to discuss the research.

Best,

Cameron Stanfill, CFA, Lead Analyst, Venture Capital

PitchBook research (part of Morningstar) reports on private equity and venture capital. We always enjoy the read.

————————————————–

CHARLES SKORINA & COMPANY

Our services: recruit CEOs & CIOs, advise on performance and pay, M&A consulting

Our clients: board members, family offices, and institutional asset managers

(520) 529-5677

News, Interviews, Research for Institutional and Family Office Investors

Prior

JPMorganChase – Institutional credit, lending, risk management

Ernst & Young – Financial systems consulting

US Army – Russian Linguist, Japan

University of Chicago, MBA, Finance

Michigan State University and

Middlebury Institute of International Studies at Monterey

Culver Academies

Read More »Angela Miller-May, new CIO at Illinois Municipal Retirement Fund (IMRF)

by charles | Comments are closed12/01/2021

Angela Miller-May, new CIO at Illinois Municipal Retirement Fund (IMRF)

11yrs Chicago Teachers’ Pension, 13 yrs Fiserv, MBA, DePaul, BA Northwestern

Read More »Investment Performance 2021: As Good As It Gets

by charles | Comments are closed12/01/2021

The good news is that, according to the current administration, the rich will pay for everything.

The bad news is that, according to the current administration, you’re rich.

— P. J. O’Rourke

Institutional investors delivered once-in-a-lifetime investment performance for fiscal 2021, from about 25 percent at the sleepiest public pensions to 65 percent at Washington University, St Louis.

As the late standup comedian Jackie Mason used to quip, “these are returns even the mafia can’t get.”

Take the eight Ivy endowments, for example. Their performance soared from a tepid 6.28 percent average a year ago (and ten-year 9.52 percent) to a sizzling 41.75 percent for fiscal 2021 as our chart below shows.

{kind=link}

As of June 30, 2021, the S&P 500 tallied a twelve-month total return of 40.79 percent against the Barclays Agg ETF return of minus 0.3 percent. Even a plain vanilla 70/30 portfolio rang up about 26 percent.All things equity had a run for the ages, but how long can it last?

Private-market-heavy, risk-on endowments, foundations, and pensions enjoyed their best performance ever, thanks to eye-popping venture capital and private equity returns and good old-fashion leverage.

But here’s the caveat, if history teaches us anything, it’s that nothing lasts forever, be it empires or bull markets. Everything ends, the only question is when.

And now here’s the bad news

According to Preqin, the unrealized portion of global venture-capital portfolios skyrocketed to $1.33 trillion by March 2021, up from $803 billion in December 2019.

How are multi-asset institutional investors going to handle their asset allocations over the next few years when venture capital marks are up 80 percent, yet nothing is being realized (where’s the cash?) and investment staffs have planned for VC commitments in the 15 percent to 25 percent range.

As Sam Gallo, CIO at the University System of Maryland Foundation puts it, what do you do when an overvalued asset class takes over your book, eats up your risk budget, and threatens your ability to continue allocations across the entire portfolio? Meanwhile, every VC manager and their cousin is raising a new fund every month and if you don’t re-up, they will never let you in again.

Here’s another pickle. Let’s say a pension or endowment lays on a one percent bitcoin position that jumped to eight percent overnight. Should they rebalance back to one percent so as not to reduce their allocations to other asset classes?

Or what if bitcoin drops fifty percent as it has done at least seven times in the past, cutting that new eight percent allocation down to four percent of book?

Endowments and pensions are supposed to be long term investors, so in theory they should hold on to that bitcoin position.

But keep in mind that CIOs get bonuses by minimizing tracking error relative to their benchmarks, especially on the downside. No board likes to miss benchmarks by more than two percent a year.

What to do?

Read More »{kind=link}