When I was young I thought that money was the most important thing in life; now that I am old I know that it is. — Oscar Wilde

An exceptional, highly successful family office client and I were discussing the differences in generations a while back and he characterized the divergences this way.

“Charles, my brothers and I slept two to a room in a tract home and sat at the family table each night for dinner. We grew up with a common set of values and beliefs. We have worked together all our adult lives, and I can’t remember the last time we had an argument. But our kids grew up rich, in separate households, with different friends and a diverse mix of views. We got an allowance, our kids have trust accounts.”

Next-gen heir-do-wells

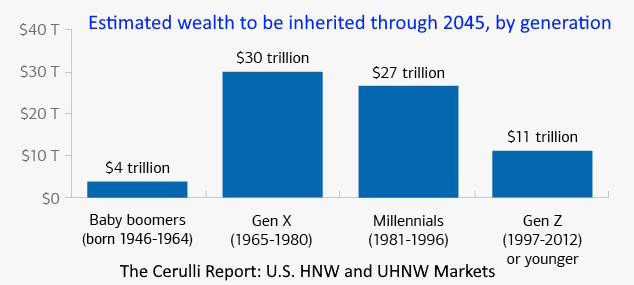

We’ve all heard by now that the next several decades will see the “greatest transfer of wealth in history with $84 trillion expected to pass down to younger generations.” But what are the implications for asset and wealth managers? How are these next-gen heir-do-wells any different than prior generations?

Estimated Wealth to be Inherited

{kind=link}

The UHNWs

At the heart of the wealth management mother lode runs the ultra-high-net-worth seam, households with net assets over $30 million. These denizens of El Dorado may represent just a sliver of the population – one half to one percent – but they control almost a third of the investable assets.

Altrata/Wealth-X estimates that about ninety percent of the current North American UHNW contingent are entrepreneurs and hands-on operators, mostly self-made men and women who are accustomed to being in control.

These wildly successful entrepreneurs have a hard time understanding what institutional CIOs do or why anyone would waste their time investing that way. Most would side with Andrew Carnegie, who once advised the students of Curry Commercial College in Pittsburgh, Pennsylvania to “put all your eggs in one basket, and then watch that basket.”

Different ages, different apps

Capgemini’s latest wealth report 2024, highlights the challenges of servicing this wealth tsunami, describing these next-geners as principled, passionate, and looking for more than just cents on the dollar. They are also comfortable with technology.

These digital immigrants, natives, and nomads want their assets globally accessible, kept safe, and managed well, but unlike prior generations they don’t always need or want human contact.

The London-based KnightFrank Group notes that “we’re talking about a cohort that is seeking a wealth manager who is on their wavelength, if indeed they want to deal with a human at all.”

As an aside, an executive at a major west-coast software company told me recently that technology is moving so fast that age groups (and the firm’s employees) just a few years apart use completely different apps to connect and interact. From text to TikTok in the blink of an eye.

Mission-based, promise driven

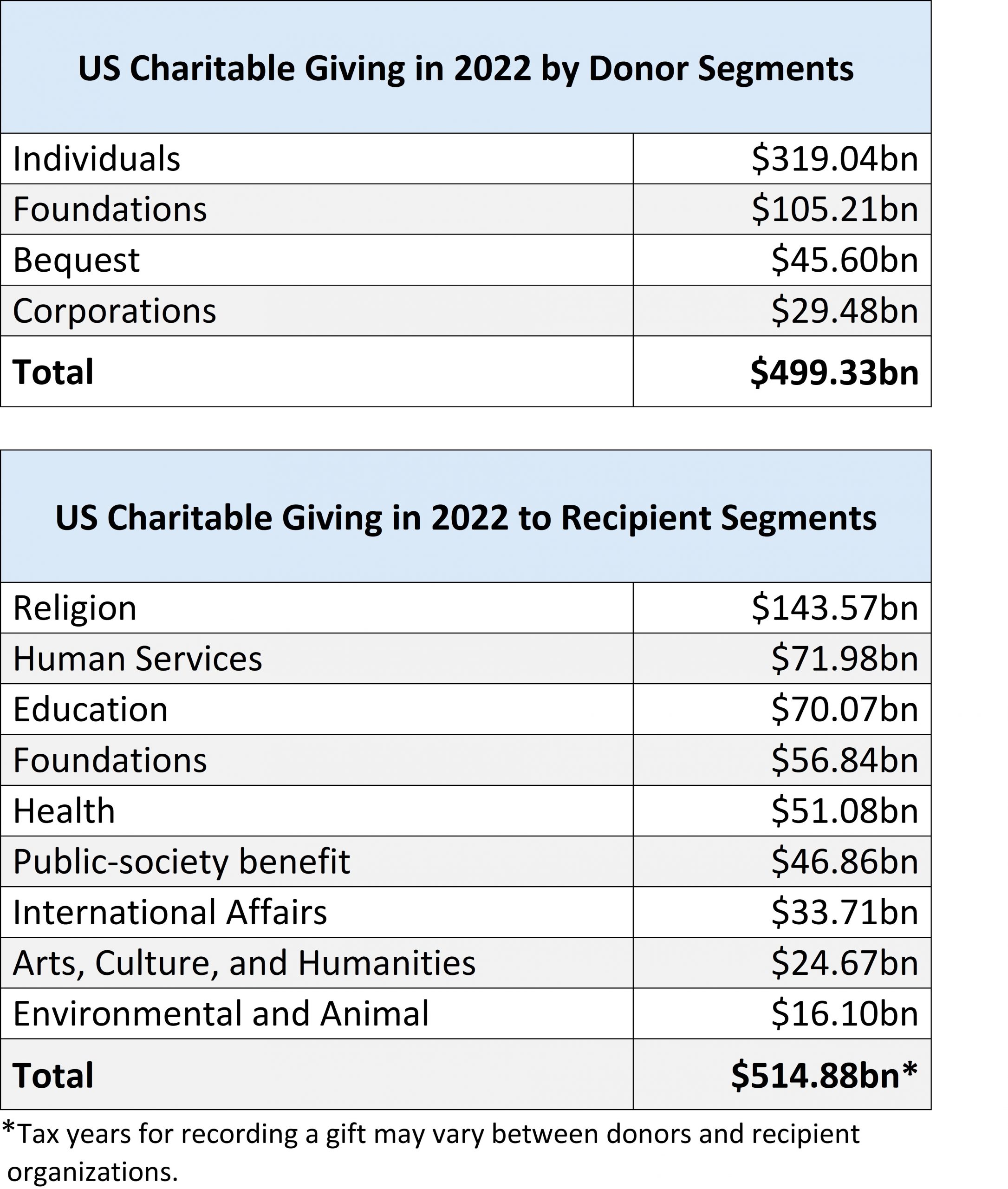

Americans by nature are a generous people giving almost half a trillion dollars to charity in 2022. UHNWs topped the list, contributing almost five percent to total individual donations of $319 billion. But that’s not all.

The UHNW cohort cares deeply about their causes and they drive foundation formation which, in turn, gave an additional $105.21bn in 2022. There are well over 100,000 private foundations in the U.S with AUM totaling about $1.4 trillion, 3,300 of these have AUM over $50 million.

The next generation of philanthropists will want help from their advisors as they align their investments with their philanthropy.

Suzanne Brenner, partner and former chief investment officer at Brown Brothers Harriman, puts it this way “research shows millennials are twice as likely to invest in companies that make a positive impact. It’s important that we understand not only what they want to do, but that we all understand what defines success.”

Jon Hirtle, executive chairman of Hirtle Callaghan, describes the commitment to mission-based wealth management as promise driven.

“We promise our families that we will continue to live in a certain way, we promise to support the causes we care for and often we promise to help provide for our children and grandchildren.”

Here’s a breakdown of those promises in the two charts below. Data from the Lilly Family School of Philanthropy, Indiana University.

US Charitable Giving in 2022 by Donors/Recipients

{kind=link}

Final thoughts

Seventy-eight percent of the Ultras surveyed by Capgemini consider value-added services essential to a solid wealth management relationship. Among them, concierge services, networking opportunities, legal consultation, lifestyle advice, and investment advice across multiple jurisdictions.

But how is this much different than any other era? True, there is apparently a king-tide of wealthy next-geners about to wash up on our shores. And technology has made the sourcing and delivery of financial services convenient and attractive. And yet, it seems to us the UHNWs want what they have always wanted, help with their financial and family affairs and they are willing to pay for it. Witness our current search (posted below).

Technology and high-touch services are expensive, however. Boston Consulting Group sees wage inflation, rising costs for front-office teams, and tech spending degrading profits at asset managers with AUM under $150 billion.

Making matters worse, “investors are moving towards passively managed funds and other products that have lower fees” even as capital and labor costs increase.

Wealth management is a crowded field with established, deep-pocketed players and looming tech competitors. Think Ant Fortune or Anchorage Digital as templates for disruptive innovation.

Wall Street is littered with the bones of the complacent. It’s time to give your competitors another look. Some might make fine partners.

Postscript

One Texas based wealth manager we know wrote me the following after reading my draft.

We have a number of multi-generational clients and in my experience, they are very traditional and just want to grow their wealth. As you know, Texas is very entrepreneurial and the state is very business friendly.

I think that leads to a contrast with the old money wealth on the two coasts, which often tends to be more liberal.

We have a multi-generational client in the northeast and the daughter is a politically active Ivy League graduate. Even in that case, her only request is no energy stocks. In contrast, her brother just wants to make money!

{kind=link}