Being too far ahead of your time is indistinguishable from being wrong — Howard Marks

Our latest fiscal year-end 2024 endowment performance report features ten-year and one-year returns, and AUM for one-hundred-forty-four US and eight Canadian institutions, the latest available.

In our line of work, acquiring talent and capabilities for institutional and family office clients, we like hard data on the individuals who drive the investment decisions. Returns may be historical, but they are useful clues to an investor’s – and board’s – views, process, and discipline.

We consider a ten-year span to be a rigorous and revealing measure of the strength of an institution’s long-term investment abilities, but we remind our readers that there’s much more to the story.

Board members and administrators set the parameters for investment execution, and they are the ones to judge whether their goals are met. Every school has its own endowment payout rate and tolerance for risk and that’s what CIOs aim for. Some schools rely heavily on income, others place more weight on growing the principal.

A tale of two markets

For those institutions holding substantial U.S. public equity stakes life is sweet. As Chris Markoch at MarketBeat writes, the S&P was up twenty-three percent in 2024, “driven by earnings growth and sector leaders in AI, biopharma, and blue-chip companies.”

Sometimes it’s best to run with the herd, to paraphrase our Mr. Marks. But for endowments with heavy exposure to alts, particularly private equity, there were challenges.

PE has performed well for forty years. But there are periods when the economy tanks, deals stagnate, and returns to investors slow to a trickle.

Here’s Peter Lynch’s droll take on fickle Mr. Market, and a few partisan comments on PE from Alisa Amarosa Wood and Chris Harrington, partners at KKR, and Ludovic Phalippou, professor of Financial Economics at Saïd Business School, University of Oxford.

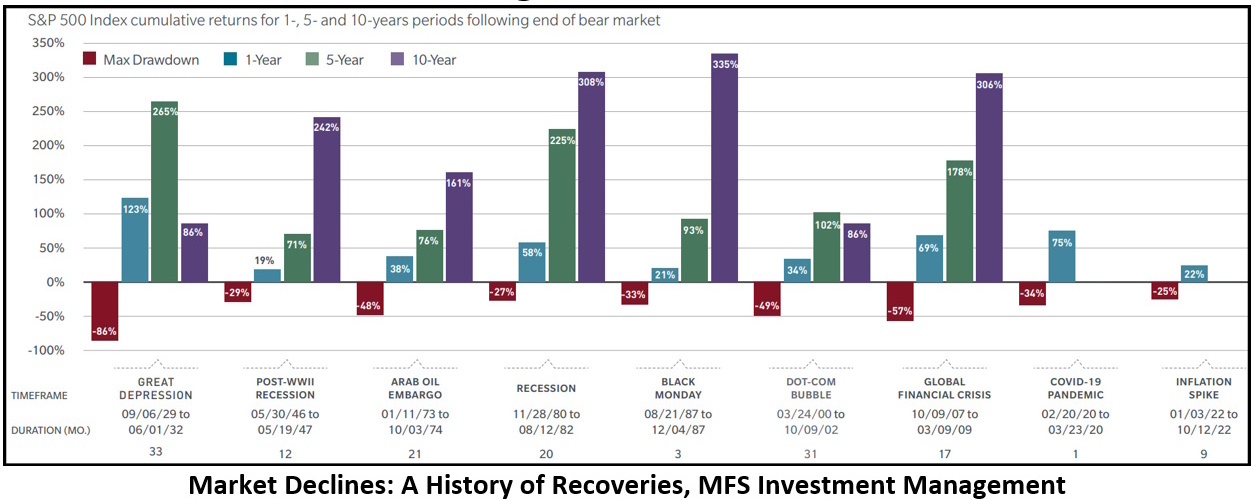

Opposing pundits aside, we take comfort in the chart below, a cheerful visual we ran in September’s newsletter from MFS investment Management depicting the S&P’s bumps and grinds.

S&P 500 Index cumulative returns for 1-, 5-, and 10-year periods following end of bear market

{kind=link}

Tenure and Turnover

What a difference a decade makes. Only about a third of the CIOs in our FY2024 endowment investment report logged ten years or more tenure, and those are mostly the ones on top.

Mr. Philip Zecher, CIO at Michigan State University, and our featured guest below, will soon pass the ten year mark and the endowment’s splendid performance reflects his time and attention.

Chief investment officers new to the position, Ms. Geeta Kapadia at Fordham for example, barely have time to roll up their sleeves and grab a pitchfork. It takes five years at least to clear, plough, and seed an endowment, and five more to fully bear fruit.

College endowments consist of thousands of gifts with strings and legally binding contracts attached. To repeat a well-worn trope, it takes years to fully implement a multi-asset, multi-generational investment strategy and altering course mid-stream – a new investment chair, a change in CIOs, court battles – can sap performance for a decade.

————————————————-

Phil Zecher, chief investment officer

Michigan State University

Count Lev Nikolayevich Tolstoy maintained that history was a vast “storm-tossed sea” of individual actions – complicated, unpredictable, impossible to fathom.

When it comes to the stock market, our thoughts exactly.

In the world of institutional investing, another vast and unpredictable expanse, there always seems to be a handful of hot hands who enjoy spectacular runs, but most shine within an era or a set of conditions and then they’re gone. That does not mean their efforts were wasted.

The good Count’s gloomy perspective aside, we think CIOs can and do make a difference. Take Mr. Phil Zecher, for example, Ph.D. Nuclear Physics from Michigan State University, and for the last ten years, chief investment officer at the MSU endowment.

In the years since Mr. Zecher took on the CIO role, the university’s endowment performance has steadily improved. MSU’s ten-year return in our latest report rests comfortably at number eight on our list of one-hundred-and-nineteen over one billion AUM segment, a praiseworthy effort.

Pensions & Investments recently took note. “Among the 44 endowments whose returns have been tracked by Pensions & Investments as of Nov. 11, the median return was 9.8%. The top performer was Michigan State University’s endowment. The East Lansing, Mich.-based $4.4 billion endowment returned a net 15.1% for the fiscal year ended June 30, 2024.”

Mr. Zecher is not cut from common endowment cloth. Over half of all endowment and foundation chief investment officers come from other nonprofits. Mr. Zecher, on the other hand, rocks a hard science and Wall Street risk background.

After earning his doctorate from MSU, (BS, Physics, Ohio University) he worked at Deloitte in NYC, co-founded a risk analytics firm, sold it, then joined a hedge fund as partner. He began advising the MSU endowment in 2011 when I met him and eventually became the university’s first CIO.

It’s been pretty much uphill ever since, barring the rocky tenure of recent MSU presidents and a gymnastics scandal, the “annus horribilis” of MSU yore.

We spoke with Mr. Zecher about the endowment’s laudable performance, what he has done to focus the portfolio, and how he looks at the world of institutional investing.

Skorina: I think we first began chatting when you were sitting on the endowment advisory board and it’s been quite an odyssey since. What led you from the halls of science to the temples of Mammon?

Zecher: I used to joke that I was trying to find a career by process of elimination. But the reality was simpler, I wanted to live in NYC and there weren’t many nuclear physics jobs in NYC.

I think studying physics is a great education, and I’d do it all over again, the analytic skills you develop are broadly applicable to many problems, not just physics. In one sense, physics problems are perhaps a lot easier than problems involving people.

Skorina: Your mission when you became CIO in 2016 was to build a team, pull together a strategy, and make the school some money. How did you begin?

Zecher: Complicated questions, Charles. As you mentioned, I had been on the board’s investment advisory committee for a number of years and that was really my introduction to the allocator space (I’m embarrassed to admit I bought Swenson’s book but have never read it).

During that time, I was frequently frustrated by the “received wisdom” that was offered without analytical appraisals as basis for our actions. As a research scientist by training, I tend to be skeptical of just about everything I hear without supporting data.

And to be clear, the data often does not give you a clear answer, but it might shed light on how shaky the ground is you’ve built your edifice on. Once we had a team in place – thank you for your search assistance, Charles – we started to carefully evaluate a lot of the implied assumptions our portfolio rested on.

We wanted to test our funds against those assumptions. To do that meant we needed to remove a lot of the common biases that come with how people generally evaluate managers. That led us to do a blind review of the portfolio, which included our IC, where we removed all the identifying information for managers and simply showed how the manager performed against various assumptions – no names, track records, strategy or asset class labels etc.

We try to be students of behavioral science, appreciating how easy it is to be biased by information that is not important. For instance – I don’t always succeed, but – I try to ban us looking at any time series graphs. Why? Humans are very good at creating totally plausible stories to explain purely random data.

Skorina: Any surprises?

Zecher: Yes and no. I wasn’t surprised that a lot of the funds didn’t hold up to the assumptions we’d made about them, or about the role they played in the portfolio. But I was surprised at how consistent the reviews were from the team and IC. There were a few funds with mixed reviews, but most of them clearly either met or failed to meet expectations.

It took us a couple of years to clean house, and there were certainly some missteps along the way, but today we have over twice the assets and about half the number of [public] funds we started with.

Skorina: Most CIOs at endowments and foundations work from a standard template these days. How do you keep a fresh perspective?

Zecher: You can only keep a fresh perspective if you are constantly critical of what you are doing. Which is hard, and even harder when you’re being successful.

For me, being a late comer to the field helps me keep an outsider mentality. The dogma that comes from learning something earlier in your career is very hard to overcome.

An example of that dogma is most asset models. Your “standard template” or pejoratively, bucket filling models, lead teams to focus on beating their bucket, not necessarily doing what is right for the whole portfolio. That puts the responsibility on the IC to ensure that they have the right buckets to best benefit the total portfolio.

Our earlier process of critically evaluating our asset allocation model led us to throw out the buckets and adopt more of a risk-budgeting approach—perhaps not surprising since I’d grown up on the risk side of the business rather than the trading or allocator side.

You could also describe our approach as more like the “total portfolio approach” used by the Australia Futures Fund or New Zealand Superannuation Fund.

Every investment is evaluated by what it contributes to the whole portfolio’s return and risk.

Skorina: How do you spend your time, managing, investing, teaching, stakeholder relations? I’m not certain that boards and administrations always understand what CIOs do.

Zecher: Yes, all of those. I guess you could say we work very hard to do nothing. We are, after all, long-term investors, so we shouldn’t be messing around with the portfolio too often. But to keep our mettle, we need to constantly monitor and evaluate options, even if nothing comes of most of that work.

The CIO’s role, like any role with a lot of responsibility, turns towards making sure all the stakeholders understand and are aligned with the strategy.

As Ellen Shuman, former CIO at Carnegie Corporation, once told us at a Greenwich Roundtable meeting, when you become CIO the focus shifts from investing to management, policy, and politics.

Skorina: The endowment had an impressive year as of June 30, 2024. How did that happen?

Zecher: In investing there is always some combination of luck and skill involved. And a little bit of luck early can help a lot later on—luck is after all a compounding asset.

What probably differentiated and benefited us over other institutions in the last year, has actually benefited us over a number of years, and that is an intentional move towards more U.S. centric global equities.

In the 2017-2018 timeframe we debated a basic question, did we believe foreign markets were likely to be stronger or better performers over the next decade or two than the U.S? Our answer was and remains no.

For instance, consider how much has been invested in European companies over the last few decades based on uncritically applying U.S. corporate valuation models to European companies.

According to these models, Europe has been and remains “cheap”. But taking our valuation models and applying them to foreign markets belies an appreciation for culture differences, among other risks.

Again, take Europe, banks play a much bigger role in corporate finance than in the U.S., and corporate leaders often don’t see their job as just to increase stock value, like they do in the U.S. That is not to say there aren’t opportunities in foreign markets, but they require fine brush work, not the broad brush of the asset allocation models.

Skorina: What are your thoughts about future opportunities?

Zecher: Today, we think one of the most important, and little discussed, mega trends is how value has shifted from physical capital to intellectual capital.

Most physical production has become commoditized, and with any commodity product, margins get squeezed to nothing and the only way you can survive is through scale.

Consider NVIDIA, which has become one of the most valuable companies in the world but has no foundry, only a massive amount of very hard to replicate IP. If IP is going to be where the value is, it is going to be what drives outside returns.

If IP is the future of wealth, then it’s not surprising that Google’s research budget alone is 5 times the entire National Science Foundation’s budget, and slightly more than the National Institute of Health’s budget. If you are concerned about wealth disparity, that should concern you.

Skorina: It’s been a pleasure speaking with you. Any closing comments?

Zecher: I love the university and – yes, I’m biased – our world class physics department. And I feel privileged to be in a position to help MSU. Hopefully, for many years to come. Go Green!

————————————————–

Endowment Performance 2024

How we display our data

We have grouped our endowment performance data into four sections:

- 119 US endowments over $1bn

- 22 US endowments, $500mm to $1bn

- 3 US endowments, non-June 30 FYs

- 8 large Canadian endowments in $CA dollars (about $0.70 US dollar)

Eleven endowments over $1 billion and four between $500 million and $1 billion are managed by OCIO firms (Outsourced Chief Investment Officer). We have highlighted them in green.

Caveats

There is no agreed upon standard for endowment performance reporting and no institutional body to enforce a standard even if there was one.

Many schools report their numbers net of all costs including external management fees, internal office costs, and the endowment tax, but not all. Some report gross returns. Others subtract external management fees but not office costs or the endowment tax. Over a ten-year period that makes a difference.

Another issue. Timing of returns can be a big problem, particularly over the last few years. Public market results are computed and consolidated by investment custodians and reported to their clients usually within a month of the fiscal close.

But things get cloudier for illiquid alternative assets with no quoted prices: so-called “level 3” items. As a result, private market valuations take much longer, three months at least, and there is a fair amount of wiggle room.

Most investment teams will not know their June 30th private investment performance until September 30th or later. In some cases, much later. As a result, returns released to the media are estimates at best.

Where are the women?

We count twenty-one female investment heads, or 19%, within our over one billion AUM group and two of fifteen, about 13%, in the $500 million to $1 billion group. There are two women among the eight Canadian endowments. We have highlighted them all in blue.

Despite excellent performance across the board and an almost fifty-fifty split in the ranks below CIO, it is still a tough road to the top.

————————————————–

Updates and edits

Try as we might, there are bound to be errors. Please let us know. We will make the changes and send out an update in a few weeks.

To all those who helped us, thank you. We greatly appreciate it.

Best regards, Charles

(download newsletter as PDF) (download league tables as PDF)

{kind=link}