If I disagree with something, I either bet against it, or I keep silent – Amarillo Slim

It’s been a festive fifty years for the alternative investment industry, with private equity the belle of the ball. And as Chuck Prince, former CEO of Citigroup once remarked, “as long as the music is playing, you’ve got to get up and dance.” But no matter how compelling the party, there are usually a few contrarians lingering in the wings.

Ken Frier, CEO of OCIO firm Atlas Capital Advisors, wrote recently that “The signs are clear, the non-profit model, where the energy goes toward selection of alternative investment managers, is bearing less fruit.

That’s the case even for the Yale endowment – their performance beat a simple 90/10 stock/bond index portfolio by 6.2% in 1994 – 2004, by 3.6% in 2004 – 2014 and just 1.2% in 2014 – 2024. And that 1.2% in the past decade is overstated since Yale cannot sell their private holdings at the reported value.”

Maybe so, but with private equity forecast to double from $5.8tn in 2023 to $12.0tn in 2029 and the “barbarians” storming the retail 401(k) ramparts, one can’t help but wonder what the smart money is up to. As Ben Carlson, A wealth of common Sense, quipped, “being a contrarian is easier in hindsight.”

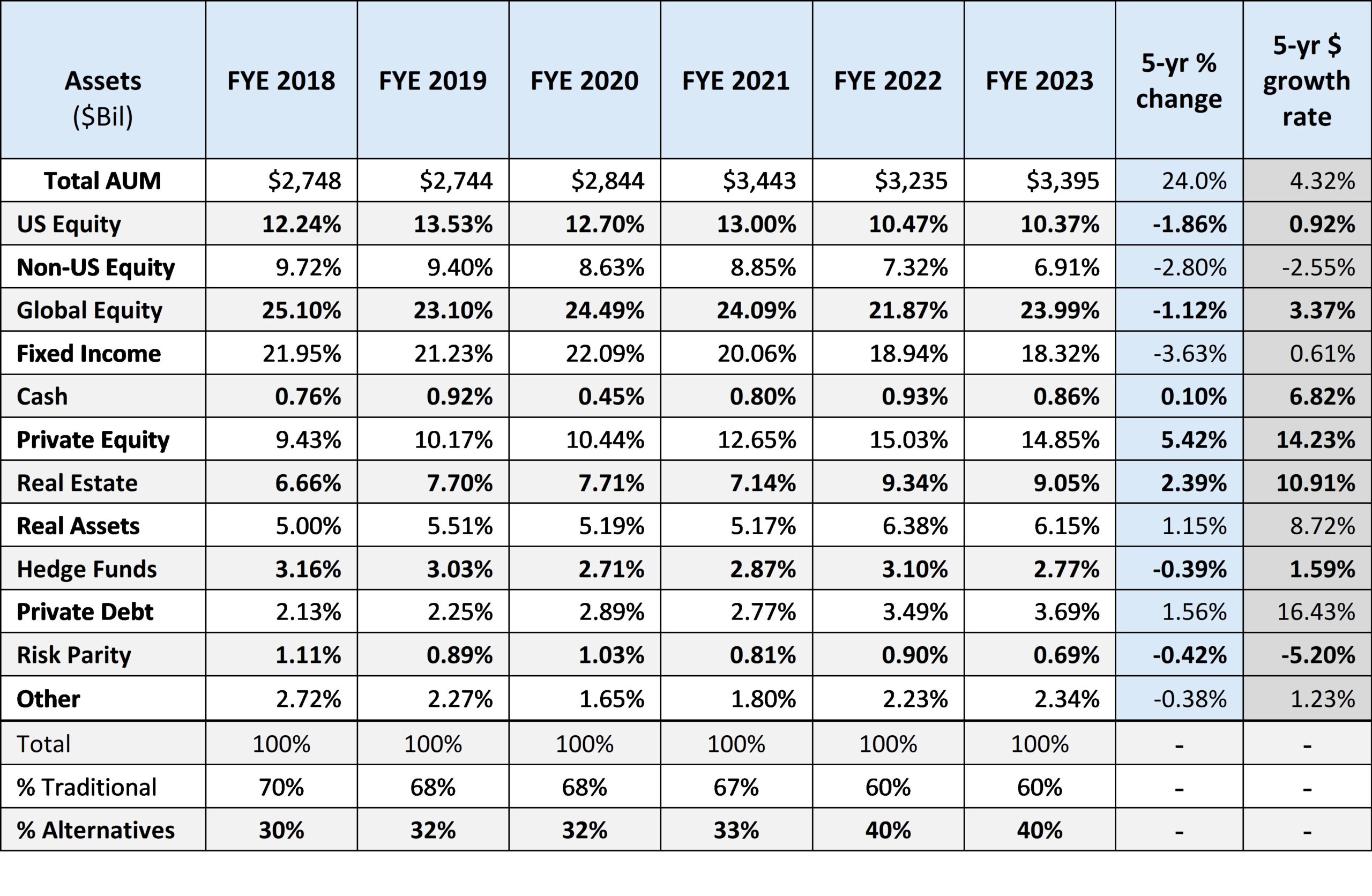

Most big dollar state pensions still follow the herd. CalPERS recently announced they’re going large on private assets with a target 40% allocation, about $225 billion of the $563 billion dollar fund.

As for CalPERS peers, Stephen L. Nesbitt, CEO & CIO of institutional consultant Cliffwater reported last year that allocations to alternatives reached 40% of state pension assets in 2022, with PE at 14.85% as of 6-30-23.

State Pension Allocations

June 30, 2018 to June 30, 2023

{kind=link}

Non-profit Investment staffs try their best, but most go to the same conferences, use the same consultants, follow the same trends, and invest with the same managers as their peers. Career risk is too great to “think different” when politicians and media trolls lie in wait for any and every mistake.

Pinching pennies

Despite the grumbling, fees still don’t seem to matter much to the institutional crowd. Richard Ennis, former co-founder of consulting firm EnnisKnupp (now AON), thinks the herd pays too much for too little.

“Alts bring extraordinary costs but ordinary returns – namely, those of the underlying equity and fixed income assets.” Ennis finds big endowments in his study – estimated to hold 65% of assets in alternative investments – fare worse than pensions, which have a 35% exposure.

When compared with a market index that he designed with a specific stock-bond mix to mimic funds’ risk profile, endowments have trailed by 2.4 percentage points annually in the 16 years through June 2024. Over the same period, pensions undershot their benchmark by 1 percentage point a year.”

Callan recently published their 2025 Cost of Doing Business Study – “a comprehensive look at the investment management fees paid by institutional investors.” Here are a few highlights from the press release:

“Total investment management fees averaged 40 basis points (bps) across all asset pools. But this headline figure masked significant variation across investor types:

- Nonprofits continued to pay the most, averaging 57 bps, driven by larger allocations to alternatives.

- Public funds averaged 43 bps, but the largest plans resembled nonprofits in both structure and fees.

- Corporate funds averaged 30 bps, driven by growing use of liability-driven investing (LDI).

- Insurance pools, with their conservative asset allocations, were the lowest at 20 bps.”

To be fair

As Howard Marks pointed out in a recent memo to clients, the last decade has not been easy for chief investment officers, given the extraordinary swings in markets and sentiment.

To loosely quote Mr. Marks, we have experienced an economic recovery and bull market of record duration thanks to historically low interest rates, followed by three radical shocks – a once-in-a-century pandemic, economic closure, and unprecedented rescue measures.

This, in turn, led to surging inflation and the fastest interest rate rise in history. And yet, despite all this, we are currently witnessing a rare economic soft landing accompanied by a massive two-year stock market rally. Whew.

Back to basics

Ages ago, I took a turn on the term loan desk at Chemical Bank placing seven-year notes secured by African infrastructure projects. Most US banks at the time had little interest in such exotic paper, but the notes delivered steady returns and they worked out just fine for the bank.

Today it’s seems like “déjà vu all over again.” One of my clients, McMorgan & Company, an institutional asset manager, has a relationship with the infrastructure investment arm of OMERS and other large Canadian infrastructure investors. Low volatility, steady returns. Not much has changed. Maybe traditional stability, income, and diversification isn’t so bad.

“Serious investing is about consistency,” explains Jon Hirtle, executive chairman of Hirtle Callaghan, “and if only we could invest in retrospect we would simply pick which asset performed best last year and capture high returns with absolute certainty. But we can’t, so we diversify to generate complementary cash flows that rise and fall at different points in the economic cycle.”

Of course, how we judge consistency depends in part on our time horizon. In a paper entitled “The Rate of Return on Everything, 1870-2015,” the authors looked at Bills, Bonds, Equity, and Housing for sixteen countries over the last 145 years. Their conclusion?

“In terms of total returns, residential real estate and equities have shown very similar and high real total gains, on average about 7% per year. Housing outperformed equity before WW2. Since WW2, equities have outperformed housing on average, but only at the cost of much higher volatility and higher synchronicity with the business cycle.”

United States US Dollar returns

1.45% – Bills

2.26% – Bonds

8.39% – Equity

6.03% – Housing

(1) See Table A.10 USD returns by country, pg. A67

(2) Dataset in study covers nominal and real returns on bills, bonds, equities, and residential real estate in 16 countries from 1870 to 2015.

In other words, build a house, buy some stock, and check back in fifty years. Slam dunk if you have the time.

Final thoughts

After the last few decades of “everything everywhere all at once” with little sign of a let-up, Mr. Ben Carlson perhaps best captures the smart money zeitgeist:

“Look, I’m not saying you should always follow the trend. Of course that can be terrible advice, especially at the extremes. I just know that I’m not smart enough to know when the current cycle will end.

Therefore, I’m going to avoid going to either extreme – I’m not going all-in exclusively on everything that’s worked well in the recent past just like I’m not going all-in betting against those same recent winners by trying to be a contrarian.

Some investors are more comfortable trying to be a hero.

I’m more comfortable diversifying and admitting my limitations.”

— Charles Skorina

{kind=link}