It’s Harder Than You Think

by charles | Comments are closed02/18/2025

Too many people think investing is easy – Warren Buffett

Guest commentary: Jon Hirtle

Executive Chairman, Hirtle Callaghan

Most universities distribute about 4.5 to 5 percent of their endowment’s value each year to support school operations. The investment office therefore must earn a bare minimum 4.5 to 5 percent to maintain the nominal value of the endowment and its ability to support the university in perpetuity.

But what about purchasing power? Inflation whittles away at buying power or “real” value, so endowments add an inflation component to their earning targets. The average inflation rate since World War Two has been 3.65 percent, a cumulative price increase of 1,653.36%. So, 8 percent would seem to be the minimum return required.

But it’s not that simple. Schools have faced massive cost pressures for years. According to Mercer, “Over the past 40 years, the inflation rate in the US higher education space — as measured by the Commonfund Institute’s Higher Education Price IndexTM (HEPI) — has exceeded the headline inflation rate as measured by the Consumer Price Index (CPI) by almost 40% on a cumulative basis.”

Given this uncertainty, prudent endowment boards aim for returns that include some growth in the capital, at least another 1 percent a year on average to cover contingencies and development. All things considered – operating expenses, financial aid, growth, and the unexpected (Covid cost schools billions) – we think a 9 percent hurdle rate is a more realistic goal.

What to do?

Capital market theory assumes that “the greater the risk that an investment may lose money, the greater its potential for providing a substantial return. Setting aside the historically strong stock market returns over the last decade (and two bear markets in 2020 and 2022) , “since 1950, public stocks have, on average, produced about 6 percent over inflation with one major caveat, there’s lots of price volatility along the way. (Chart: S&P Historic Performance.)

Over that same time horizon, investment grade bonds have on average produced a scant 2 percent over inflation, albeit with far less volatility.

So why not hold 100 percent stock portfolios? The problem is the above-mentioned volatility. The stock market experiences dramatic price drops from time to time, destabilizing budgets and generally scaring the hell out of trustees.

How about adding bonds to dampen drawdowns? Not so fast. Investment grade bonds are indeed far less volatile, but with real returns of only 2 percent, not close to what institutions need.

The Capable, Independent Investment Office

Welcome to my world. How can we capture real endowment returns that exceed what is required while actively managing downside risk? Here’s how we look at it:

We source and select a myriad of compelling investments that complement each other by rising and falling in price at different times, then assemble them in a way that captures stock-market-like returns with something like bond market volatility.

This is no small task. It requires a team of experienced professionals collaborating closely and, ideally, working inside an independent investment office with substantial power.

Only the largest universities have the resources to support such an office. Most endowments and foundations do not. David Swensen described the choice as between “those that are set up to make high-quality active management decisions and those that aren’t.”

Governance Alpha

There is yet another challenge. When endowments fail to achieve their required return over time, the investment staff or the Investment Committee or both are accountable. “Alpha” is investment jargon for value added or subtracted by active investment decisions.

Governance Alpha is a term that we coined years ago to differentiate the impact of committee or CIO decisions from those made by underlying specialist money managers. Just like Manager Alpha, Governance Alpha can be either positive or negative.

When an endowment fails to earn its required return, it is most often the result of Governance Alpha, well-documented behavioral tendencies, present in all humans, which challenge retail investors and endowment committees alike.

For example, “Recency Bias” encourages committees to chase recent returns. Without a seasoned and savvy CIO with the power to check those tendencies, Governance Alpha often turns negative. That’s why a professional and independent investment operation is so important.

The OCIO solution

OCIO firms offer the proven performance of the best large institutional and family investment offices. And they have the resources, talent, structure, and process to deliver those required returns and cope with operational and regulatory burdens and the complexity of modern portfolios.

—Jon Hirtle

Read More »The 8% solution

by charles | Comments are closed02/03/2025

Activity is the enemy of investment returns —Warren Buffett

Endowment board members tell us their schools must earn at least eight percent on average to support operations and administration, student aid, and capital conservation. Unfortunately, that’s a tough nut to crack based on recent performance.

Only forty-two of the one-hundred-nineteen funds over one billion AUM in our latest FY2024 endowment performance report achieved eight percent or more over the most recent ten-year period. Roughly one third. The average return for the entire group was seven-point-seven percent.

Even worse, just one of twenty-two endowments between five hundred million and one billion in our report beat the eight percent hurdle. Sadly, those are usually the ones that most need the income.

NACUBO-Commonfund will publish their annual report in a few weeks and we will see how their endowment universe performed. But for FY 2023 NACUBO reported an average return of seven-point-seven percent net of fees for all participating schools. Not much has changed.

The NACUBO chart below shows the volatility of 10-yr returns year by year from 2002.

Here’s the problem: over the last three decades most large endowments have tried to mimic the “Yale model.” But there was only one David Swensen, and he was an outlier, a different thinker, a trailblazer and his first book was called Pioneering Portfolio Management for good reason. It was all new stuff. Forget public markets. Spend your time uncovering private opportunities with less visibility and more upside. And get in early.

The School of Swensen produced many top-flight acolytes, but the master is gone and the world has changed. Today that trail he cut through the wilderness has become a freeway and the endowment model is a very crowded trade. Let’s let Mr. Swensen explain the conundrum.

I figured out when I revised Pioneering Portfolio Management that the most important distinction isn’t between the institutional investor and the individual. It’s between those that are set up to make high-quality active management decisions and those that aren’t.

The investment management world is a strange place in that the right solution is not in the middle. The right solution is at one extreme or the other. One end of the spectrum is being intensively active. The other is being completely passive.

If you end up in the middle, which is where almost everybody is, you pay way too much in fees and end up getting subpar returns . . . The passive group is not nearly as big as it should be. Almost everybody should be there.

First level thinking

Read More »OCIO directory, fall 2024, what goes up?

by charles | Comments are closed11/18/2024

A lot of success in life and business comes from knowing what you want to avoid ―Charlie Munger

Our fall 2024 Outsourced Chief Investment Officer (OCIO) update features one-hundred-four service providers with pertinent particulars on each. We include names, numbers, emails, and titles of business executives at each firm ready to take your call.

Our goal is to help families and institutions locate, review, and connect with full-service discretionary outsource investment managers. Our directory makes it easy for prospective clients to reach them. No ads, no paywall, no charge.

A solid six months

For the six months ending June 30th, 2024, total OCIO AUM hit a record $4.456 trillion dollars on about $432 billion in new business, an impressive 10.73 percent gain. But it’s not quite what it seems.

{kind=link}

OCIOs and the multiverse

The OCIO business operates in two distinct realms, the mega-buck land of corporate pensions and a parallel universe of nonprofit institutions and family wealth. Pension plans focus on funding levels, risk mitigation, and cost reduction, while nonprofit entities and ultra-high-net-worth families attend to wealth stewardship, lifestyle preferences, and mission-based endeavors.

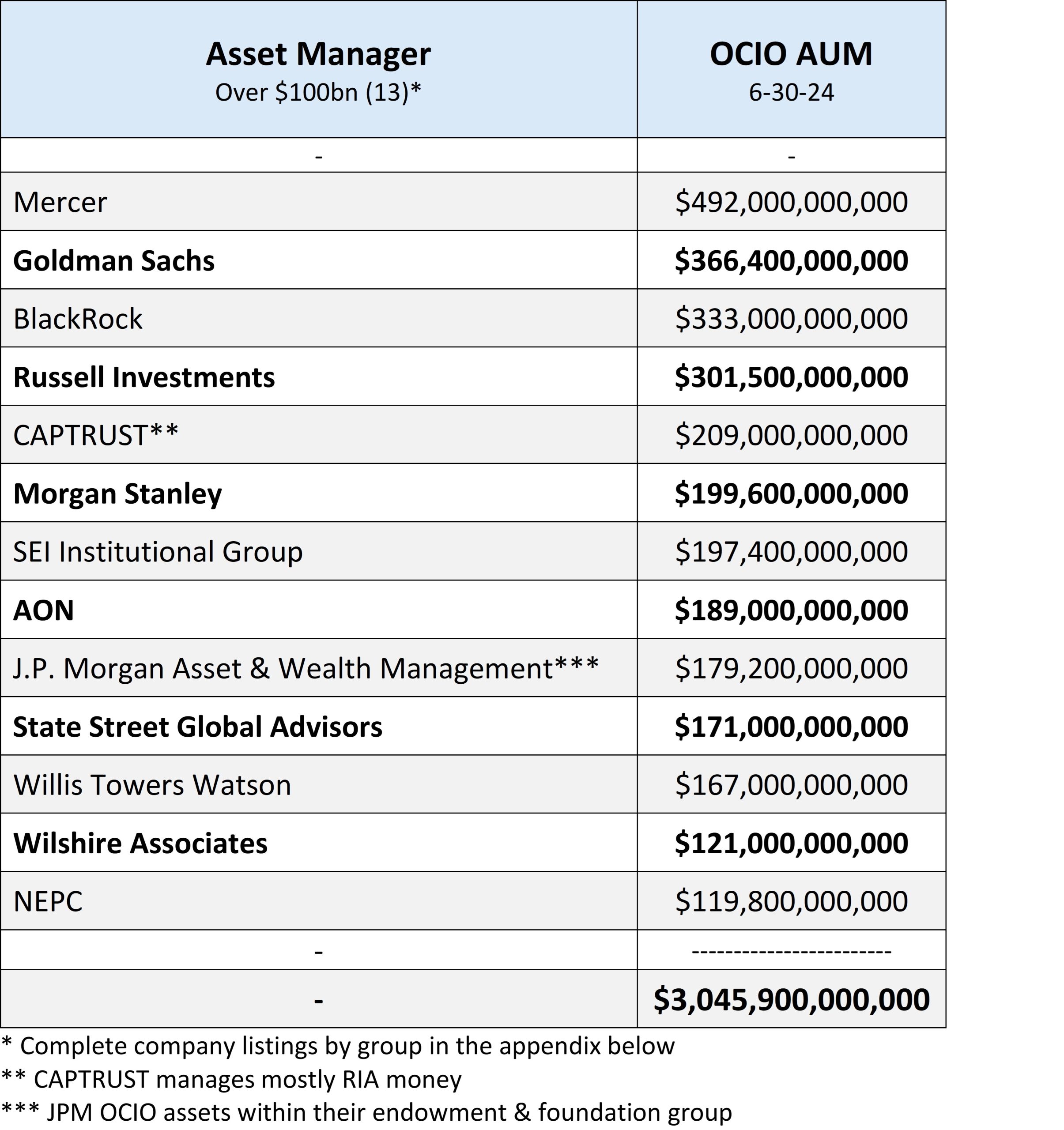

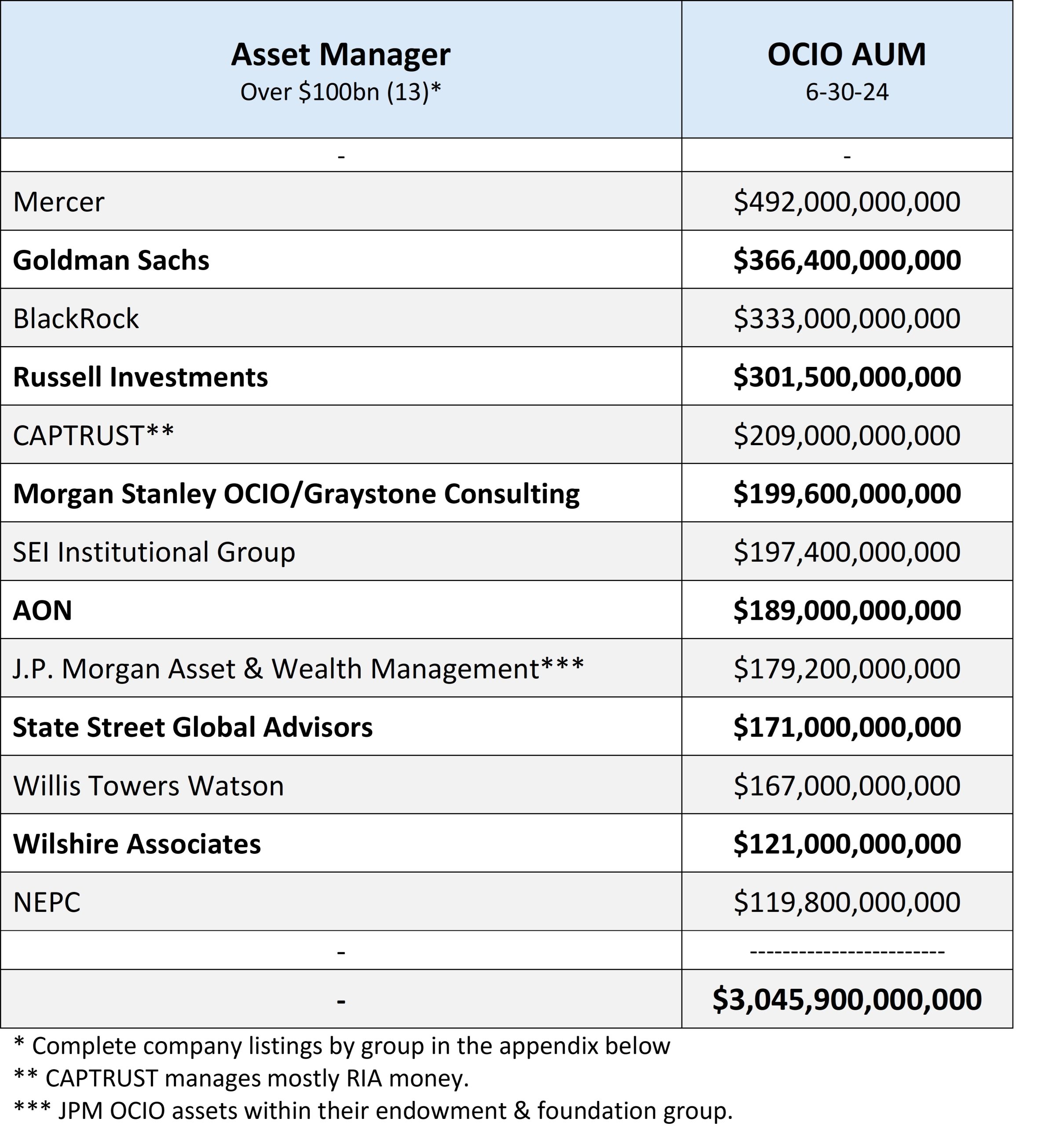

Well over half the OCIO money in our directory (probably closer to two-thirds) is pension money. This defined-benefit world is actuarial and liability driven, and heavily regulated. The largest firms with their size, resources, and appetites aggressively compete for pension money and dominate the segment, managing sixty-eight percent of our OCIO pie, about $3.046 trillion, up from sixty-four percent six months ago.

The largest firms have expertise across the board, of course, and manage substantial family and nonprofits assets, but corporate pensions are so large they skew the data.

These are big-ticket items. Recent corporate OCIO mandates include the $43.4bn UPS plan awarded to Goldman Sachs, Shell’s $30bn defined benefit pension headed to Blackrock, and Nokia’s $13.9bn plan transfer to Mercer.

(Thirteen largest OCIOs by AUM)

{kind=link}

How we report

We do not separately list pension versus nonprofit and family wealth assets for two reasons. First, the industry has no standard reporting template for OCIO assets. Pensions & Investments does their best to break out the categories, but companies can report what they want the way they want as long as regulatory requirements are met.

And second, our executive recruiting and OCIO search and selection business focuses on nonprofits, family offices, and middle-market asset managers, so we leave the mighty pension world to others.

Consolidation

This year has been a busy time for M&A. The eighty-two firms under fifty billion on our list manage about $754bn among them, mostly nonprofit and family money. However, many of the founders and original partners are aging out and because most firms are privately owned, converting equity to cash is a challenge.

But one man’s problem is another’s opportunity. Private equity firms and RIA aggregators are well aware of the challenges OCIOs face and delighted to step in with liquidity, in exchange for ownership.

Last month, RIA aggregator Hightower and wealth manager Pathstone announced OCIO acquisitions, Hightower procuring a majority interest in NEPC and Pathstone buying Hall Capital Partners.

Earlier in the year Edgehill called it quits, Agility sold to Cerity Partners, and Vanguard’s OCIO team moved en masse to Mercer. And in recent years Truvvo, Ellwood Associates, New Providence, CornerStone, PFM, and Permit Capital all decamped for better-resourced patrons. There will certainly be more.

Final thoughts

OCIO providers offer the proven performance of in-house investment staffs at a reasonable price. And they can replicate the entire investment office with the process and structure to cope with the complexity of modern portfolios and mounting operational and regulatory burden.

But fielding a full-service institutional grade practice is expensive and costs are soaring for compensation, cyber-security, audits, and compliance, to say nothing of rampant regulatory hurdles.

It takes years to fully hone systems, service, succession, and investment capabilities. Hirtle Callaghan and Blackrock opened for business in 1988, McMorgan & Company set up shop in 1969, and Brown Brothers Harriman and JPMorgan Chase hung their shingles over two hundred years ago.

Most nonprofits and family offices, basically anyone under $500 million in investable assets, don’t have the time or resources to build competitive and secure internal investment capabilities, the OCIO option is an effective and time-tested alternative.

―Charles Skorina

(download OCIO Directory as PDF)

Read More »Leadership matters

by charles | Comments are closed11/11/2024

Leadership is the capacity to translate vision into reality —Warren Bennis

Chief investment officers are C-suite executives. They manage a business that generates revenue and supports an enterprise. Be it OCIO, endowment, or family office, investment leadership matters.

We recruit these executives and facilitate OCIO selections so we pay attention to who they are, what they do, and how well they do it. Here are a few observations.

Larry Fink, CEO of BlackRock, describes leadership as “a consistent voice, a clear purpose, a coherent strategy, and a long-term view.” McKinsey defines leadership as “enabling others to accomplish something they couldn’t do on their own.” Jon Hirtle, executive chairman Hirtle Callaghan and former Marine Corps officer, considers leadership “the noble cause – serving the client.”

The authors of “What Makes a Great Leader,” list three qualities as key – architects, bridgers, and catalysts. “As architects, they build the culture and capabilities for co-creation. As bridgers, they curate and enable networks of talent inside and outside their organizations to co-create. And as catalysts, they lead beyond their organizational boundaries to energize and activate co-creation across entire ecosystems.”

Myra Drucker’s prolific CIO academy

Some years ago we spoke with Myra Drucker, the former chief investment officer of the Xerox corporate pension group, and wrote about her impressive internal CIO training program.

Notable alumni include Joseph Boateng, CIO of Casey Family Programs Foundation, MaDoe Htun, CIO of the William Penn Foundation, former endowment CIO’s Mary Cahill and Matthew Wright of Emory and Vanderbilt respectively (and founders of OCIO firms Acansas and Disciplina).

Mr. Boateng recalled that “Myra told all of us in the investment office that she would consider her job a success if she accomplished just two objectives: first, meet her performance targets for the pension fund; and second, develop all of us so well that each of us could go on to become a CIO. She is a role model I still look up to.”

When we asked Ms. Drucker for the secret to her CIO sauce, she answered this way: “First, obviously, you hire the best people you can find. Every hiring decision should be a big deal that gets your full attention.

“Then, push them. Make them stretch and take on new assignments. I rotated my people among asset classes. Nobody just sits at a fixed-income desk without ever having to deal with equities or alternatives. For every asset class and major initiative, I made sure there were two team-members assigned: a lead and a back-up.

“But it goes beyond just portfolio management. Everybody is exposed to the operational and administrative tasks. Everybody has to understand fund accounting.

“I know that some fund managers think they should be the sole interface with the board or trustees, and reserve that job to themselves. I think that’s a mistake. I made sure my people were in meetings with the board members and made presentations to them. “Managing” a board is a key, make-or-break skill for a fund manager, but if you’re not taught how to do it, how can you ever operate on that level?”

Time and money

Read More »OCIOs: reconnecting the dots

by charles | Comments are closed10/09/2024

“The true sign of intelligence is not knowledge, but imagination”

—Albert Einstein

You don’t have to reinvent the wheel to build a successful outsourced chief investment officer (OCIO) business, but it sure helps to connect the dots.

Despite countless paeans to AI these days, when it comes to OCIOs, there is very little new under the sun, and as most wide-eyed newcomers eventually come to admit, discretionary service providers are notoriously hard to scale.

Jon Hirtle of Hirtle Callaghan launched the first conflict-free, independent investment office managing family and institutional money in 1988. Forty years later, the OCIO industry is bifurcated, highly diverse, and intensely competitive with hundreds of OCIOs, RIAs, banks, brokers, and asset managers competing for discretionary customers. It’s a jungle out there.

But with the formidable forty-year swell in private equity, venture capital, credit, and infrastructure investing, OCIOs are matching capabilities with clients in creative new ways.

Dean Keith Simonton, Professor Emeritus of Psychology at the University of California, Davis, posits that “genius hunts widely—almost blindly—for a solution to a problem, exploring dead ends and backtracking repeatedly before arriving at the ideal answer.”

Boutique providers – that’s pretty much everyone under about one-hundred billion in AUM – such as Hirtle Callaghan, Commonfund, Makena, and McMorgan & Company, have spent years polishing their services and honing their competitive advantage. As the market grew and providers proliferated, firms adapted, combining traditional prix fixe solutions with selective a la carte services.

According to Cerulli Associates, “Amidst inflation, interest rate hikes, market volatility, and the changing implications of geopolitical conditions, asset owners are increasingly drawn to the OCIO model for the management of sleeves for alternatives and private asset classes for which they do not think they have the appropriate level of expertise.”

It’s all about access

Access to the crème de la crème of alternative managers challenges most tax-exempt institutions and family offices, but OCIOs, with the diversified endowment model as their template, have spent years sourcing and cementing relationships with top private equity and venture capital professionals. Providers now offer a variety of alternative sleeves for those who prefer specialized participation.

A few prescient firms have gotten even more creative. McMorgan & Company, for example, has an infrastructure fund not common in boutique outsourcers.

A few years ago, the company established a relationship with OMERS Infrastructure, the infrastructure investment arm of OMERS, a large Canadian pension plan that has been investing directly in infrastructure since 1999. This relationship has led McMorgan to create a fund which co-invests in certain deals alongside OMERS Infrastructure.

There’s nothing new about infrastructure funds, plenty of firms in the mix, but few boutiques take the time to build something special. The McMorgan Infrastructure Fund hews a path for prudent tax-exempt and family office investors.

Final thoughts

We’re in the executive search business, for those that haven’t already guessed, along with OCIO search and selection and the occasional consulting assignment, so job seekers send us resumes and call almost every day.

Most candidates hammer on about what they’ve got and what they want. Surprisingly few spend much time asking about what our clients want, the folks we care most about.

But now and then someone applies that “second level thinking” Howard Marks talks about. They surprise us by connecting the dots, by carefully researching a potential employer and asking, what does this company need and how can I give it to them, rather than ramble on about what they, the job seeker, wants.

Here’s an example, a story we heard some while back.

Read More »{kind=link}