Following Next-Gen Money

by charles | Comments are closed06/17/2024

When I was young I thought that money was the most important thing in life; now that I am old I know that it is. — Oscar Wilde

An exceptional, highly successful family office client and I were discussing the differences in generations a while back and he characterized the divergences this way.

“Charles, my brothers and I slept two to a room in a tract home and sat at the family table each night for dinner. We grew up with a common set of values and beliefs. We have worked together all our adult lives, and I can’t remember the last time we had an argument. But our kids grew up rich, in separate households, with different friends and a diverse mix of views. We got an allowance, our kids have trust accounts.”

Next-gen heir-do-wells

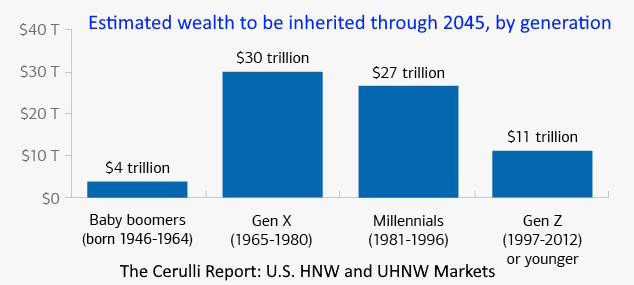

We’ve all heard by now that the next several decades will see the “greatest transfer of wealth in history with $84 trillion expected to pass down to younger generations.” But what are the implications for asset and wealth managers? How are these next-gen heir-do-wells any different than prior generations?

Estimated Wealth to be Inherited

{kind=link}

The UHNWs

At the heart of the wealth management mother lode runs the ultra-high-net-worth seam, households with net assets over $30 million. These denizens of El Dorado may represent just a sliver of the population – one half to one percent – but they control almost a third of the investable assets.

Altrata/Wealth-X estimates that about ninety percent of the current North American UHNW contingent are entrepreneurs and hands-on operators, mostly self-made men and women who are accustomed to being in control.

These wildly successful entrepreneurs have a hard time understanding what institutional CIOs do or why anyone would waste their time investing that way. Most would side with Andrew Carnegie, who once advised the students of Curry Commercial College in Pittsburgh, Pennsylvania to “put all your eggs in one basket, and then watch that basket.”

Different ages, different apps

Capgemini’s latest wealth report 2024, highlights the challenges of servicing this wealth tsunami, describing these next-geners as principled, passionate, and looking for more than just cents on the dollar. They are also comfortable with technology.

These digital immigrants, natives, and nomads want their assets globally accessible, kept safe, and managed well, but unlike prior generations they don’t always need or want human contact.

The London-based KnightFrank Group notes that “we’re talking about a cohort that is seeking a wealth manager who is on their wavelength, if indeed they want to deal with a human at all.”

As an aside, an executive at a major west-coast software company told me recently that technology is moving so fast that age groups (and the firm’s employees) just a few years apart use completely different apps to connect and interact. From text to TikTok in the blink of an eye.

Mission-based, promise driven

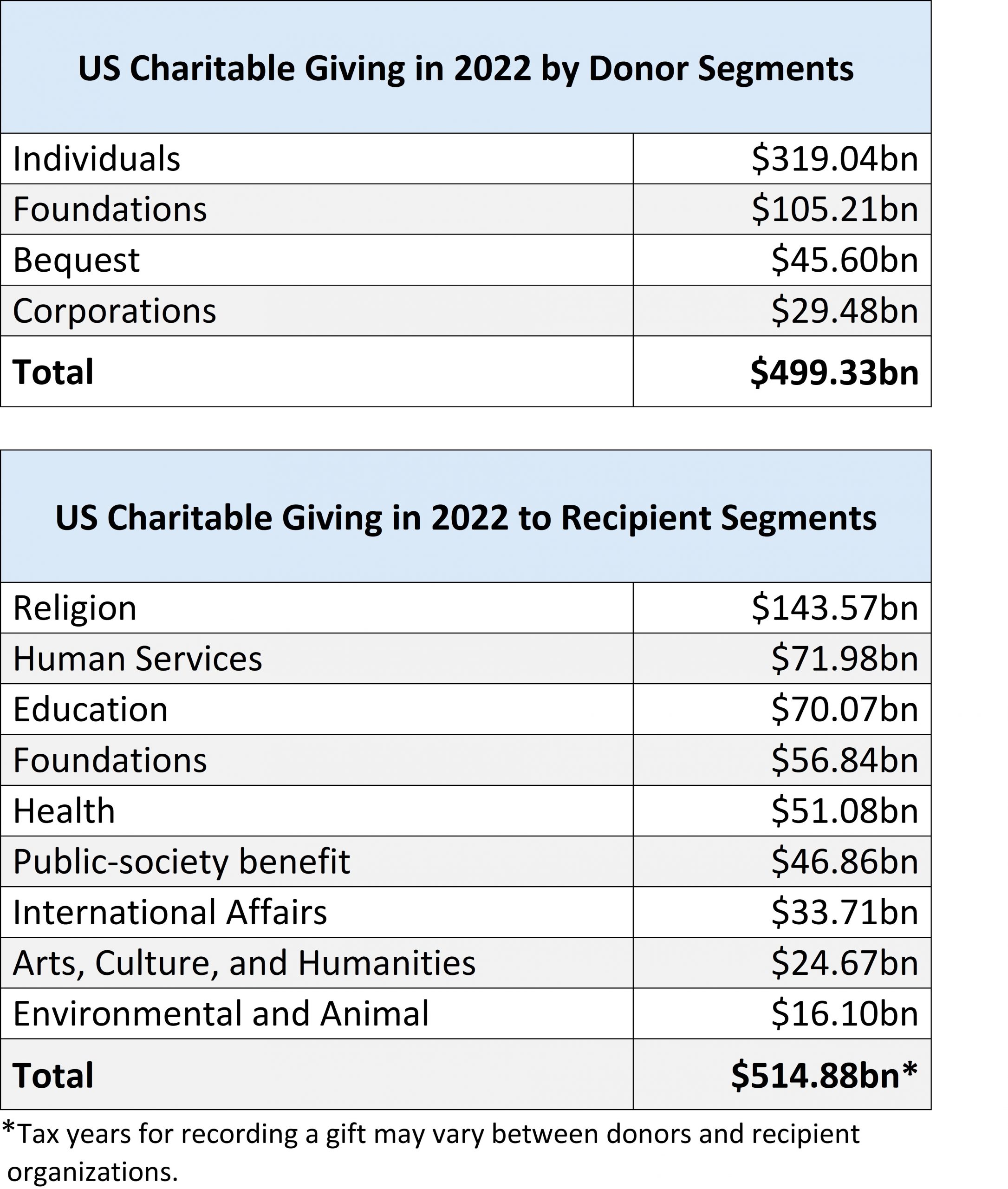

Americans by nature are a generous people giving almost half a trillion dollars to charity in 2022. UHNWs topped the list, contributing almost five percent to total individual donations of $319 billion. But that’s not all.

The UHNW cohort cares deeply about their causes and they drive foundation formation which, in turn, gave an additional $105.21bn in 2022. There are well over 100,000 private foundations in the U.S with AUM totaling about $1.4 trillion, 3,300 of these have AUM over $50 million.

The next generation of philanthropists will want help from their advisors as they align their investments with their philanthropy.

Suzanne Brenner, partner and former chief investment officer at Brown Brothers Harriman, puts it this way “research shows millennials are twice as likely to invest in companies that make a positive impact. It’s important that we understand not only what they want to do, but that we all understand what defines success.”

Jon Hirtle, executive chairman of Hirtle Callaghan, describes the commitment to mission-based wealth management as promise driven.

“We promise our families that we will continue to live in a certain way, we promise to support the causes we care for and often we promise to help provide for our children and grandchildren.”

Here’s a breakdown of those promises in the two charts below. Data from the Lilly Family School of Philanthropy, Indiana University.

US Charitable Giving in 2022 by Donors/Recipients

{kind=link}

Final thoughts

Read More »OCIO update, spring 2024, a Record Run

by charles | Comments are closed05/18/2024

4400 registered foals, and only 16 or 18 of them make it to the Derby ― John Sosby, Claiborne Farm

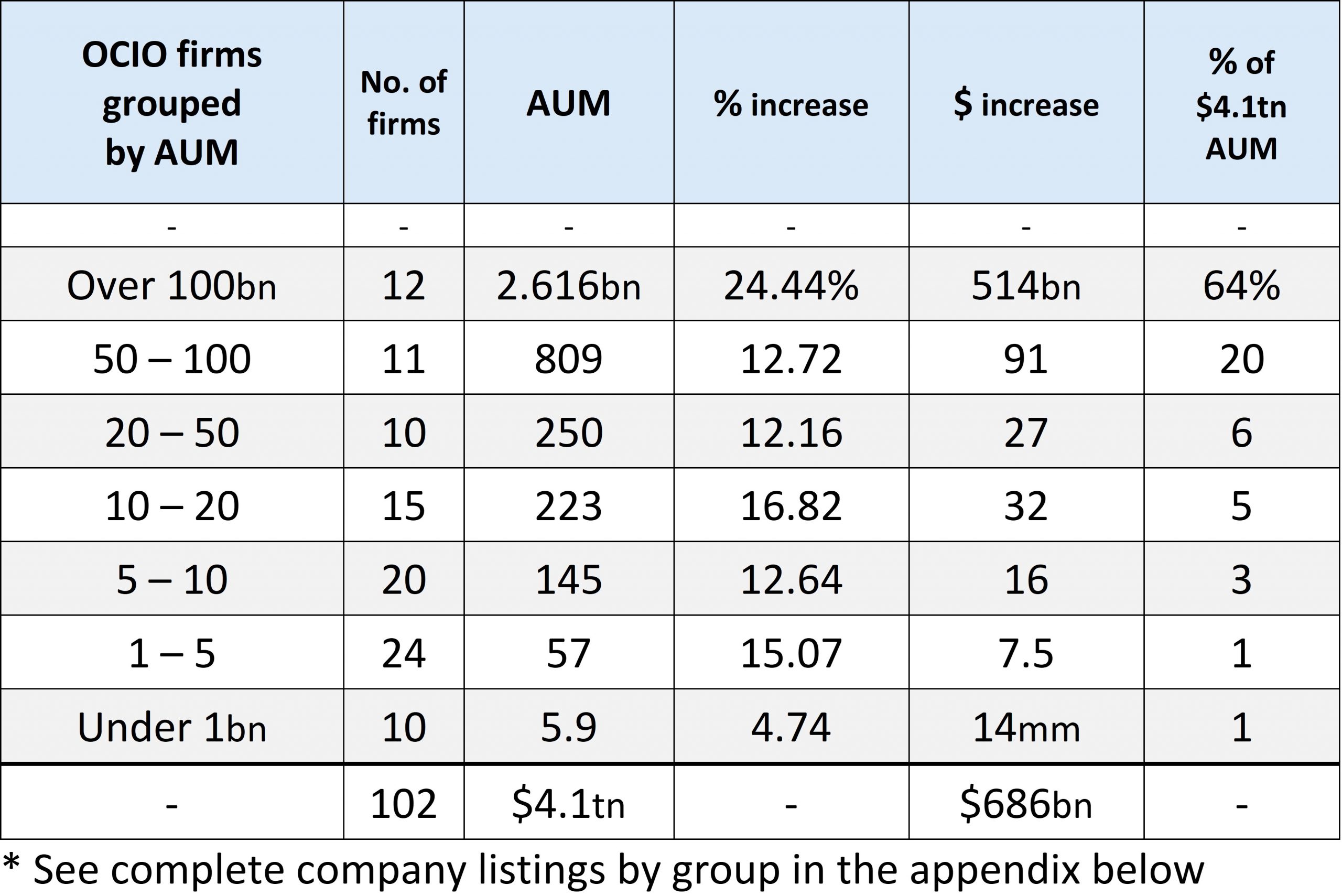

What a year. For the twelve months ending December 31st, 2023, total outsourced AUM managed by the one-hundred-two firms in our latest OCIO Directory reached a record $4.1 trillion dollars thanks to $686 billion in new business, a whopping twenty percent increase.

This chart shows which OCIOs gained the most AUM for the year. We grouped the firms by size, numbers per group, and growth in dollars and percentage.

{kind=link}

Winner takes all

Here’s what caught our attention. Less than a quarter of the firms on our list manage most of the money, about $3.4tn, while the other seventy-nine outsourcers divvied up the remaining $681bn. The twelve largest OCIOs alone control over $2.6tn or sixty-four percent of the outsourced total.

As for new business in 2023? Almost three-quarters of last year’s gain accrued to these twelve largest providers, thirteen percent went to the next eleven, and those dogged seventy-nine fought for the remaining twelve percent, roughly $83bn.

The Twelve

$420,000,000,000 – Mercer

$329,400,000,000 – Goldman Sachs

$319,000,000,000 – BlackRock

$243,200,000,000 – Russell

$193,500,000,000 – SEIC

$182,100,000,000 – MS Graystone

$169,800,000,000 – CAPTRUST

$164,200,000,000 – J.P. Morgan

$163,000,000,000 – WTW

$157,000,000,000 – State Street

$155,000,000,000 – AON

$121,000,000,000 – Wilshire

As in past years, the largest source of new OCIO mandates in dollar terms came from corporate pensions.

For most OCIOs, however, the corporate defined-benefit world is a land apart and out of reach, actuarial, regulated, and liability driven, with big-ticket AUM on offer. According to the latest Milliman corporate pension report, the top 100 US DB plans held about $1.32 trillion in assets in 2023.

By the way, only four of these plans outsourced their DB obligations during the year, so there are still a few mandates to be had.

Many firms, many flavors

Each OCIO has its own culture, investment style, and biases. Some firms focus on indexing and liquid markets, others on alternatives, still others on ESG. Some customize portfolios, others don’t.

But biases affect risk, allocations, and outcomes. Alternatives including venture capital and private equity have outperformed in the past and may do so again.

A 2022 University of Chicago paper concludes that “Venture capital performance remains remarkably persistent across funds raised by the same general partner. In contrast, buyout funds’ performance persistence becomes noticeably weaker over time.”

However, there’s a trade-off in liquidity and transparency. If it’s liquidity you want, check the fine print for lockups, redemptions, gates, and fees.

“The top LBO funds invest money quickly, but the liquidation of portfolio companies is a long process, requiring more than 12 years from the vintage year,” according to Jeffrey Hooke, senior lecturer, Johns Hopkins University.

Before choosing an OCIO, know which way they lean.

Failure to communicate

Here’s one last point to keep in mind.

Our spring 2024 OCIO Directory

(download OCIO Directory as PDF)

Read More »The OCIO Mirage

by charles | Comments are closed05/03/2024

The outlook wasn’t brilliant for the Mudville nine that day: The score stood four to two, with but one inning more to play … Casey at the Bat, Ernest Lawrence Thayer

Hope springs eternal in the OCIO space. Each year confident investment officers and ardent marketeers announce their brand-new best-in-class discretionary outsourced solution. But for most of these eager rookies, few customers will come or care.

Looking back over the last four decades, the best time to pitch an outsourced chief investment officer (OCIO) proposition was probably about thirty years ago when prospects were plentiful, competitors few, and margins were healthy.

In today’s hyper-competitive wealth management arena, fielding a full-service institutional grade asset management team is expensive and costs are soaring for compensation, cyber-security, audits, and compliance, to say nothing of rampant regulatory hurdles and those nasty unknown unknowns.

(See our charts below for detailed office cost breakdowns.)

We recently completed an OCIO search and selection engagement for a sizable east coast nonprofit and found all the responding providers to be consummate professionals and serious competitors.

Firms such as Hirtle Callaghan, Blackrock, J.P. Morgan, and Brown Brothers Harriman, among the stalwarts in our directory, have had years to hone their systems, service, succession, and investment capabilities. But it’s never easy.

In an interview with Jon Hirtle for our 2020 OCIO review he reminisced on the firm’s early efforts to win clients.

Debby [Jon’s wife] and I often talk about the financial low point when our checking account had dropped to $17. What kept us going was that everyone loved the OCIO concept. The idea of powerful, informed, energetic advocacy without the conflicts of interest that define the traditional investment industry.

This Cold Cruel World

It’s tough for newbies and niche players to keep up with the veterans. This year kicked off with Edgehill calling it quits, Agility selling to Cerity Partners, and Vanguard’s OCIO team decamping en masse for Mercer.

They’re in good company. The past few years have seen a steady stream of outsourcing hopefuls merge with better-resourced patrons including Truvvo, Ellwood Associates, New Providence, CornerStone, PFM, and Permit Capital. There will certainly be more.

Boston Consulting Group, in their Global Asset Management 2023 review, estimates that – due to rising costs – the industry’s compound annual growth rate in profits “will be approximately half the average of recent years (5% versus 10%).”

Most nonprofits and family offices, basically anyone under $500 million in investable assets, don’t have the time or resources to build competitive and secure internal investment capabilities.

Investment Office Costs: you pay to play

Strategic Investment Group published an investment office cost study recently, Building Blocks and Costs of an Internal Investment Office, that’s worth a read.

Read More »Endowment Performance 2023: You never see them coming

by charles | Comments are closed02/27/2024

I worried about so many things during my life, but the really tough hits I never saw coming. — Anonymous

Our 2023 endowment performance report features ten-year investment returns for one hundred thirty-eight US and eight Canadian institutions, the latest available. In addition, we include one-year returns for 2023, 2022, 2021 along with AUM, as of their respective fiscal year-ends.

NACUBO and Commonfund released their annual endowment study two weeks ago chock full of facts and figures. Chief among them, the 688 participating U.S. college and university endowments and affiliated foundations returned 7.7 percent, net of fees, for fiscal 2023. Trailing 10-year returns averaged 7.2 percent.

NACUBO noted that “Historically, institutions with larger endowments often have secured better one-year investment results than those with relatively smaller endowments. The reverse occurred in FY23, owing to smaller institutions’ substantially larger allocations to publicly traded securities.”

All this is nice to know, but in our line of work, acquiring talent and capabilities for institutional and family office clients, we like hard data on the individuals who drive the investment decisions. Returns may be historical, but they are useful cues to an investor’s process and discipline.

As it turns out, of the 688 institutions in the NACUBO study, including 138 endowments over one billion AUM and 77 between $500 million and a billion, only about a third have an internal chief investment officer or designated investment head, mostly those in the above mentioned half a billion and up categories. These are the ones that catch our eye. The rest use OCIOs, investment committees and consultants, RIAs, brokers, and well-meaning volunteers.

The lay of the land

Institutional investors had a lot on their minds the last few years: Covid and a market crash in 2020, meme stocks and valuation- frenzy in 2021, war and rates in 2022, and bank busts in 2023. But other than the specter of rate increases, no one saw these disruptive outliers coming.

And yet, the best investors somehow find a way to outperform. After years of recruiting investment talent, we’ve observed that top performers tend to stay on top, despite the occasional speed bumps.

Cambridge Associates concurs. In a 2022 paper on investment advice for the entrepreneurial mindset, CA studied equity portfolio managers over a twenty-year span and found that, “On average, “successful” managers underperformed about one quarter of the time over any rolling three- and five-year periods.”

Unfortunately, it’s hard to find good data on nonprofit CIOs with twenty years or more of tenure, but ten years is doable. Hence our emphasis on ten-year performance.

We also list the current endowment CIO or designated head of investments, although often performance was baked in by the prior CIO.

Paula Volent for example, now at Rockefeller University, was for twenty years the CIO at Bowdoin College and her fingerprints linger on Bowdoin’s latest 11.7% ten-year return, topping our charts yet again.

Where are the women?

Read More »It Takes Guts

by charles | Comments are closed01/23/2024

The cautious seldom err or write great poetry. – Howard Marks’ favorite fortune cookie, Dare to Be Great II

J.P. Morgan Chase is king of the realm these days, but during my time at Chemical Bank there were other big dogs walking the “Street.”

The neoclassical, money-minting, “House of Morgan” sat kitty-corner to our headquarters at 20 Pine.

Next door, David Rockefeller’s baronial fiefdom, the sixty-story, glass and steel slab, One Chase Manhattan Plaza, towered over Chemical’s pre-war high-rise while Jean Dubuffet’s tangled abstract, Group of Four Trees, flipped us off from the courtyard.

And uptown, Manufacturers Hanover lent to the corporate elite from their Park Avenue perch, eyeing with distain Chemical’s middle-market rabble. While high above the fray, Walter B. Wriston’s Citicorp lorded it over us all.

But in the end, Chemical smelled blood, devoured their unwary prey, and for desert had its way with the Morgan name. If you can’t beat them, eat them. J.P. would understand.

That thing called “edge”

Mark LaMonica, Director of Product Management at Morningstar, describes the elusive, hard to define attribute called “edge” as better information, analytics, or behavior. But no one in the investment industry ever built a great business without another edge we call “guts,” the confidence and courage to take a chance.

With vast, industry-wide reserves of talent and resources, the odds of any single firm vaulting organically over the competition are slim to none without disruptive technology, blockbuster products, or an unbeatable track record.

But, disruptive technologies and blockbuster products – computers or ETFs – come around maybe once every fifty years, as Angelo Calvello points out in Institutional Investor. And, while consistent, multi-decade investment superiority isn’t impossible, it’s exceedingly rare.

Promises kept

Jon Hirtle, executive chairman of OCIO firm Hirtle Callaghan considers investment management a mission and describes the stewardship of client wealth as “promise-driven” investing.

When we ask our clients which risk matters most, they almost always place “mission failure” at the top of the list. Serious investors care deeply about keeping their promises.

Those promises can be tallied up to calculate a “required return.” Achieve that required return and we can fulfill our promises; fail to achieve it and we are likely to disappoint the people and causes we love.

But here’s the challenge. To endure and deliver on those promises made, which course can overcome the all-too-common clutch of complacency?

M&A or the highway

Read More »{kind=link}