Changing Times

by charles | Comments are closed10/13/2025

“People don’t know what they want until you show it to them.” — Steve Jobs

The late David Swensen, Yale’s formative chief investment officer, found value in dark corners, those unknown managers and overlooked opportunities Heather Gillers referred to in a recent WSJ article. But there hasn’t been much new in money management since Mr. Swensen wrote the playbook.

Whether non-correlated, factor-based, or managed TPA, when we do our ten-year return studies most institutional portfolios look and act the same.

So, here’s a question. If most investment managers think alike, what’s to keep AI and algorithms from taking their jobs?

Barter to Bitcoin

Disruptive technologies and blockbuster products, computers and ETFs, come around maybe once every fifty years, so the time seems ripe for the next big thing — those creative convulsions Professor Clayton Christensen warned about.

Here’s a piece that caught our eye, an excerpt from an article on AI, crypto, and seismic change by Caltech grad and tech founder Ryan W. Sinnet, PhD. A vignette about horses.

In 1920, America reached peak horse: 25 million animals powering the nation’s economy.

But the end had already begun in the cities. In 1910, New York City housed 128,000 working horses, according to the NYC Department of Records. They pulled carriages, delivered milk, hauled freight.

Every morning, thousands of horses trudged through Manhattan streets, their iron shoes striking cobblestones in a rhythm that had echoed through cities for centuries. Smart money owned stables, carriage companies, hay distribution networks. The horse industry wasn’t just big—it was civilization itself. Unthinkable to replace.

Yet by 1920—even as rural America reached peak horse—New York’s horse population had already collapsed to 56,000, more than half gone in a single decade. The transformation was already accelerating.

By 1912, New York City had 38,000 motor vehicles on its streets, and the automobile age had clearly arrived. By 1917, the last horse-drawn trolley made its final trip.

The entire ecosystem that supported horse labor—stables, blacksmiths, harness makers, feed suppliers, auction houses—didn’t evolve or adapt. It vanished. The 25 million horses that powered America in 1920 plummeted to just 3 million by 1960.

Those horses never came back.

Relationships matter

Chatbots, robo-advisors, Zoom, and the cloud are now obligatory parts of the financial landscape. Generations born in the internet age seem fine without the human touch as long as their assets are globally accessible, secure, and earn enough to pay the bills.

But that’s on the retail side. These “digital natives” may be inured to “Tilly Norwoods” and “Schwab Intelligent Portfolios,” but how about foundations, endowments, and UHNW families with large diverse holdings? Might they still want a human at the helm? Someone who “understands their needs and speaks to their sensibilities” as Ken Tsuboi, chief investment officer at McMorgan & Company describes constructive client engagement.

Successful wealth stewards embrace the goals, aspirations, lifestyle preferences, and risk tolerances of their clients. Kathryn George, Partner, Brown Brothers Harriman points out that “Wealth is never just about money. It’s intimately intertwined with relationships – between generations, between values, and between expectations.”

We tallied a record high $4.865 trillion dollars in outsourced assets In our last OCIO report. Rich Nuzum at Franklin Templeton counts the “rise of private market alternatives; the global war for in-house investment talent; the data, digital and technology arms race; and the increasing number of asset owners questioning the need to manage investments in-house” as major factors driving growth.

Funds and families with two billion or more may have the means to field internal investment capabilities, assuming they have the time and patience to build, staff, monitor, and maintain such a business. But for those with less regal sums, outsourcing the complexities and risks to professionals they trust is an effective way to keep their commitments and secure their legacy.

Final thoughts

According to Altrata’s World Ultra Wealth Report 2025 “the total net worth of the UHNW class rose by 6.7% to $59.8tn at the end of June 2025 (and by 11.6% in 2024) – a figure double that of the annual GDP of the US.”

That’s encouraging. After all, managing money is one of America’s key competitive advantages. And we recruit the managers who manage the money.

And yet . . . I can’t help but worry.

“Not because AI does everything better, but because it does enough things cheaply enough that the economics become undeniable” as Dr. Sinnet contends.

About twenty years ago, I had lunch with the EVP of Equities at a major west coast mutual fund company. A fellow University of Chicago grad, he was smart, savvy, and successful, but the lunch ended on a sour note when I remarked that Index funds and ETFs might be a problem down the road for the full-load fund business. Right comment, wrong company.

“I obviously had no idea what I was talking about,” he snapped. “These ETFs are a gimmick with a niche future at best. Clients want the human touch and always will. And they will always pay for it.”

Not so long after our lunch he left the firm – retired early I heard – and that giant fund warehouse has had a bumpy ride since.

As Andy Grove, the former CEO of Intel used to say, “only the paranoid survive.” Me? I keep looking over my shoulder.

— Charles Skorina

Read More »Smart money

by charles | Comments are closed08/06/2025

If I disagree with something, I either bet against it, or I keep silent – Amarillo Slim

It’s been a festive fifty years for the alternative investment industry, with private equity the belle of the ball. And as Chuck Prince, former CEO of Citigroup once remarked, “as long as the music is playing, you’ve got to get up and dance.” But no matter how compelling the party, there are usually a few contrarians lingering in the wings.

Ken Frier, CEO of OCIO firm Atlas Capital Advisors, wrote recently that “The signs are clear, the non-profit model, where the energy goes toward selection of alternative investment managers, is bearing less fruit.

That’s the case even for the Yale endowment – their performance beat a simple 90/10 stock/bond index portfolio by 6.2% in 1994 – 2004, by 3.6% in 2004 – 2014 and just 1.2% in 2014 – 2024. And that 1.2% in the past decade is overstated since Yale cannot sell their private holdings at the reported value.”

Maybe so, but with private equity forecast to double from $5.8tn in 2023 to $12.0tn in 2029 and the “barbarians” storming the retail 401(k) ramparts, one can’t help but wonder what the smart money is up to. As Ben Carlson, A wealth of common Sense, quipped, “being a contrarian is easier in hindsight.”

Most big dollar state pensions still follow the herd. CalPERS recently announced they’re going large on private assets with a target 40% allocation, about $225 billion of the $563 billion dollar fund.

As for CalPERS peers, Stephen L. Nesbitt, CEO & CIO of institutional consultant Cliffwater reported last year that allocations to alternatives reached 40% of state pension assets in 2022, with PE at 14.85% as of 6-30-23.

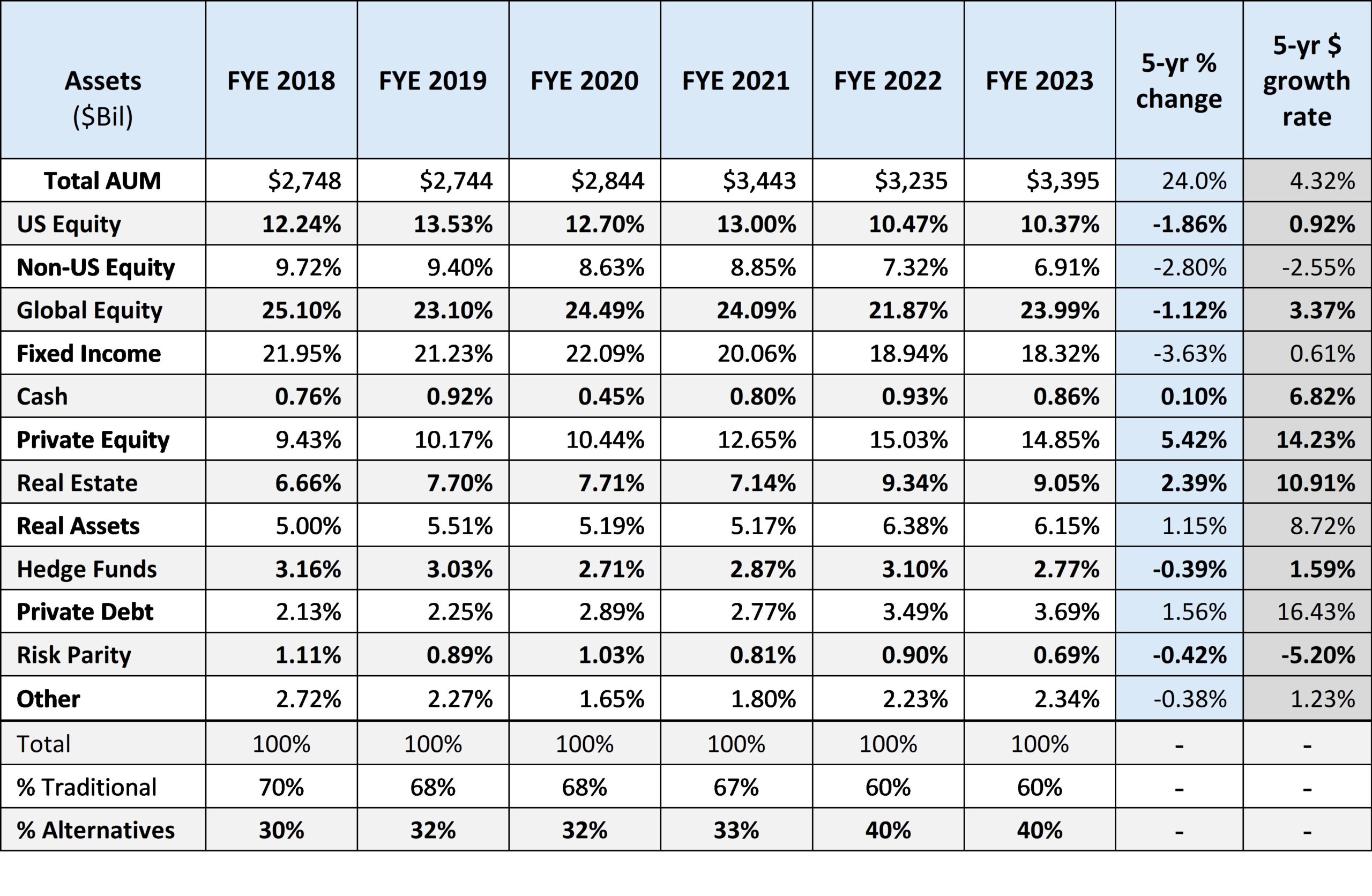

State Pension Allocations

June 30, 2018 to June 30, 2023

{kind=link}

Non-profit Investment staffs try their best, but most go to the same conferences, use the same consultants, follow the same trends, and invest with the same managers as their peers. Career risk is too great to “think different” when politicians and media trolls lie in wait for any and every mistake.

Pinching pennies

Despite the grumbling, fees still don’t seem to matter much to the institutional crowd. Richard Ennis, former co-founder of consulting firm EnnisKnupp (now AON), thinks the herd pays too much for too little.

“Alts bring extraordinary costs but ordinary returns – namely, those of the underlying equity and fixed income assets.” Ennis finds big endowments in his study – estimated to hold 65% of assets in alternative investments – fare worse than pensions, which have a 35% exposure.

When compared with a market index that he designed with a specific stock-bond mix to mimic funds’ risk profile, endowments have trailed by 2.4 percentage points annually in the 16 years through June 2024. Over the same period, pensions undershot their benchmark by 1 percentage point a year.”

Callan recently published their 2025 Cost of Doing Business Study – “a comprehensive look at the investment management fees paid by institutional investors.” Here are a few highlights from the press release:

“Total investment management fees averaged 40 basis points (bps) across all asset pools. But this headline figure masked significant variation across investor types:

- Nonprofits continued to pay the most, averaging 57 bps, driven by larger allocations to alternatives.

- Public funds averaged 43 bps, but the largest plans resembled nonprofits in both structure and fees.

- Corporate funds averaged 30 bps, driven by growing use of liability-driven investing (LDI).

- Insurance pools, with their conservative asset allocations, were the lowest at 20 bps.”

To be fair

Read More »Foundation Investing: if you’ve seen one private foundation…

by charles | Comments are closed04/18/2025

Let me tell you about the very rich. They are different from you and me. ― F. Scott Fitzgerald, The Great Gatsby

Suppose the Princeton or Yale endowment investment staff wanted to go all-in on a single stock? Forget diversification and the free lunches, just one shoot-the-moon can’t lose security. Think their trustees would go for it? Can elephants fly? Of course not.

And yet, this is the case for some of the biggest winners in the foundation world, funds like the Jen-Hsun & Lori Huang Foundation and the Lilly Endowment.

So, here’s a question. Does foundation management mirror the personalities and proclivities of their anomalous founders? And, if so, how have these various styles affected investment performance over the last five years?

For example, a preference for public markets versus alternatives, concentration versus diversification, or sports teams and crypto.

Awash in liquidity

Thanks to several extraordinary decades of wealth creation, (present speed bumps aside) private foundations and their ultra-high-net-worth benefactors are flourishing.

Over the last thirty years the number of foundations has tripled from about 40,000 in 1995 with assets of $373.4 billion to nearly 120,000 holding $1.6 trillion today.

Given a record $19.4 trillion in liquid assets in checking and savings accounts and money market funds, an S&P annual return of 9.33% over the last thirty years, and unabated philanthropic zeal among the 225,000 U.S. ultra-wealthy mega-donors, private foundations – the Getty, Casey Family Programs, the Summer Science Program – continue to play a major role in American life.

Jon Hirtle, executive chairperson of OCIO provider Hirtle Callaghan puts it this way:

Foundations are responsible for a meaningful portion of society’s accumulated and monetized patrimony. That financial patrimony is used to enhance social services, the arts, scholarship, research…human progress, if you will. So, better foundation investing means more human progress. How about that for an inspiring mission?

Ornery, reclusive beasts

Read More »It’s Harder Than You Think

by charles | Comments are closed02/18/2025

Too many people think investing is easy – Warren Buffett

Guest commentary: Jon Hirtle

Executive Chairman, Hirtle Callaghan

Most universities distribute about 4.5 to 5 percent of their endowment’s value each year to support school operations. The investment office therefore must earn a bare minimum 4.5 to 5 percent to maintain the nominal value of the endowment and its ability to support the university in perpetuity.

But what about purchasing power? Inflation whittles away at buying power or “real” value, so endowments add an inflation component to their earning targets. The average inflation rate since World War Two has been 3.65 percent, a cumulative price increase of 1,653.36%. So, 8 percent would seem to be the minimum return required.

But it’s not that simple. Schools have faced massive cost pressures for years. According to Mercer, “Over the past 40 years, the inflation rate in the US higher education space — as measured by the Commonfund Institute’s Higher Education Price IndexTM (HEPI) — has exceeded the headline inflation rate as measured by the Consumer Price Index (CPI) by almost 40% on a cumulative basis.”

Given this uncertainty, prudent endowment boards aim for returns that include some growth in the capital, at least another 1 percent a year on average to cover contingencies and development. All things considered – operating expenses, financial aid, growth, and the unexpected (Covid cost schools billions) – we think a 9 percent hurdle rate is a more realistic goal.

What to do?

Capital market theory assumes that “the greater the risk that an investment may lose money, the greater its potential for providing a substantial return. Setting aside the historically strong stock market returns over the last decade (and two bear markets in 2020 and 2022) , “since 1950, public stocks have, on average, produced about 6 percent over inflation with one major caveat, there’s lots of price volatility along the way. (Chart: S&P Historic Performance.)

Over that same time horizon, investment grade bonds have on average produced a scant 2 percent over inflation, albeit with far less volatility.

So why not hold 100 percent stock portfolios? The problem is the above-mentioned volatility. The stock market experiences dramatic price drops from time to time, destabilizing budgets and generally scaring the hell out of trustees.

How about adding bonds to dampen drawdowns? Not so fast. Investment grade bonds are indeed far less volatile, but with real returns of only 2 percent, not close to what institutions need.

The Capable, Independent Investment Office

Welcome to my world. How can we capture real endowment returns that exceed what is required while actively managing downside risk? Here’s how we look at it:

We source and select a myriad of compelling investments that complement each other by rising and falling in price at different times, then assemble them in a way that captures stock-market-like returns with something like bond market volatility.

This is no small task. It requires a team of experienced professionals collaborating closely and, ideally, working inside an independent investment office with substantial power.

Only the largest universities have the resources to support such an office. Most endowments and foundations do not. David Swensen described the choice as between “those that are set up to make high-quality active management decisions and those that aren’t.”

Governance Alpha

There is yet another challenge. When endowments fail to achieve their required return over time, the investment staff or the Investment Committee or both are accountable. “Alpha” is investment jargon for value added or subtracted by active investment decisions.

Governance Alpha is a term that we coined years ago to differentiate the impact of committee or CIO decisions from those made by underlying specialist money managers. Just like Manager Alpha, Governance Alpha can be either positive or negative.

When an endowment fails to earn its required return, it is most often the result of Governance Alpha, well-documented behavioral tendencies, present in all humans, which challenge retail investors and endowment committees alike.

For example, “Recency Bias” encourages committees to chase recent returns. Without a seasoned and savvy CIO with the power to check those tendencies, Governance Alpha often turns negative. That’s why a professional and independent investment operation is so important.

The OCIO solution

OCIO firms offer the proven performance of the best large institutional and family investment offices. And they have the resources, talent, structure, and process to deliver those required returns and cope with operational and regulatory burdens and the complexity of modern portfolios.

—Jon Hirtle

Read More »Endowment Performance 2024: How Sweet It Is

by charles | Comments are closed01/18/2025

Being too far ahead of your time is indistinguishable from being wrong — Howard Marks

Our latest fiscal year-end 2024 endowment performance report features ten-year and one-year returns, and AUM for one-hundred-forty-four US and eight Canadian institutions, the latest available.

In our line of work, acquiring talent and capabilities for institutional and family office clients, we like hard data on the individuals who drive the investment decisions. Returns may be historical, but they are useful clues to an investor’s – and board’s – views, process, and discipline.

We consider a ten-year span to be a rigorous and revealing measure of the strength of an institution’s long-term investment abilities, but we remind our readers that there’s much more to the story.

Board members and administrators set the parameters for investment execution, and they are the ones to judge whether their goals are met. Every school has its own endowment payout rate and tolerance for risk and that’s what CIOs aim for. Some schools rely heavily on income, others place more weight on growing the principal.

A tale of two markets

For those institutions holding substantial U.S. public equity stakes life is sweet. As Chris Markoch at MarketBeat writes, the S&P was up twenty-three percent in 2024, “driven by earnings growth and sector leaders in AI, biopharma, and blue-chip companies.”

Sometimes it’s best to run with the herd, to paraphrase our Mr. Marks. But for endowments with heavy exposure to alts, particularly private equity, there were challenges.

PE has performed well for forty years. But there are periods when the economy tanks, deals stagnate, and returns to investors slow to a trickle.

Here’s Peter Lynch’s droll take on fickle Mr. Market, and a few partisan comments on PE from Alisa Amarosa Wood and Chris Harrington, partners at KKR, and Ludovic Phalippou, professor of Financial Economics at Saïd Business School, University of Oxford.

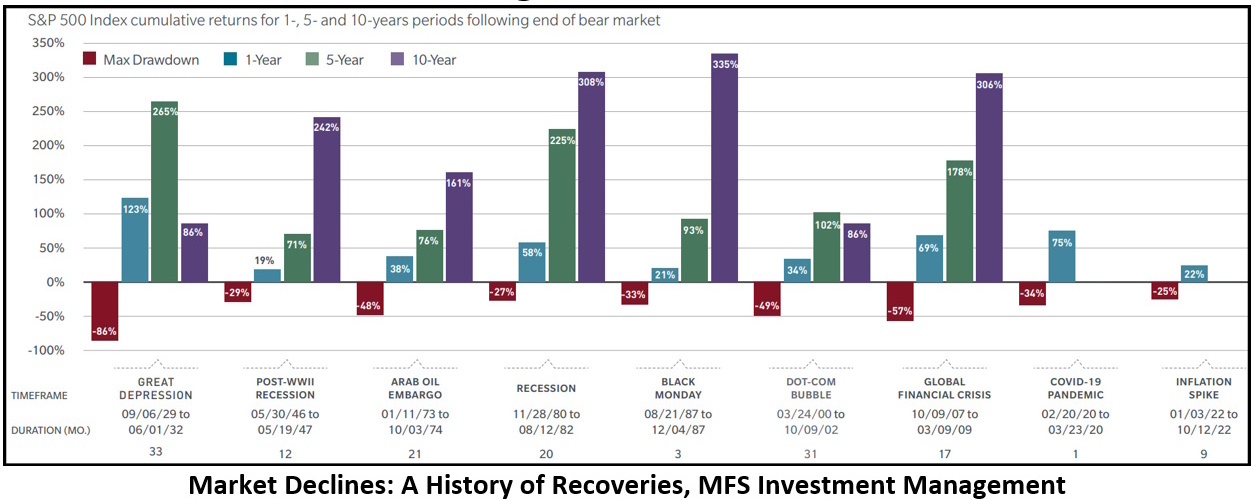

Opposing pundits aside, we take comfort in the chart below, a cheerful visual we ran in September’s newsletter from MFS investment Management depicting the S&P’s bumps and grinds.

S&P 500 Index cumulative returns for 1-, 5-, and 10-year periods following end of bear market

{kind=link}

Tenure and Turnover

What a difference a decade makes. Only about a third of the CIOs in our FY2024 endowment investment report logged ten years or more tenure, and those are mostly the ones on top.

Mr. Philip Zecher, CIO at Michigan State University, and our featured guest below, will soon pass the ten year mark and the endowment’s splendid performance reflects his time and attention.

Chief investment officers new to the position, Ms. Geeta Kapadia at Fordham for example, barely have time to roll up their sleeves and grab a pitchfork. It takes five years at least to clear, plough, and seed an endowment, and five more to fully bear fruit.

College endowments consist of thousands of gifts with strings and legally binding contracts attached. To repeat a well-worn trope, it takes years to fully implement a multi-asset, multi-generational investment strategy and altering course mid-stream – a new investment chair, a change in CIOs, court battles – can sap performance for a decade.

————————————————–

Phil Zecher, chief investment officer

Michigan State University

Read More »{kind=link}