OCIOs: reconnecting the dots

by charles | Comments are closed10/09/2024

“The true sign of intelligence is not knowledge, but imagination”

—Albert Einstein

You don’t have to reinvent the wheel to build a successful outsourced chief investment officer (OCIO) business, but it sure helps to connect the dots.

Despite countless paeans to AI these days, when it comes to OCIOs, there is very little new under the sun, and as most wide-eyed newcomers eventually come to admit, discretionary service providers are notoriously hard to scale.

Jon Hirtle of Hirtle Callaghan launched the first conflict-free, independent investment office managing family and institutional money in 1988. Forty years later, the OCIO industry is bifurcated, highly diverse, and intensely competitive with hundreds of OCIOs, RIAs, banks, brokers, and asset managers competing for discretionary customers. It’s a jungle out there.

But with the formidable forty-year swell in private equity, venture capital, credit, and infrastructure investing, OCIOs are matching capabilities with clients in creative new ways.

Dean Keith Simonton, Professor Emeritus of Psychology at the University of California, Davis, posits that “genius hunts widely—almost blindly—for a solution to a problem, exploring dead ends and backtracking repeatedly before arriving at the ideal answer.”

Boutique providers – that’s pretty much everyone under about one-hundred billion in AUM – such as Hirtle Callaghan, Commonfund, Makena, and McMorgan & Company, have spent years polishing their services and honing their competitive advantage. As the market grew and providers proliferated, firms adapted, combining traditional prix fixe solutions with selective a la carte services.

According to Cerulli Associates, “Amidst inflation, interest rate hikes, market volatility, and the changing implications of geopolitical conditions, asset owners are increasingly drawn to the OCIO model for the management of sleeves for alternatives and private asset classes for which they do not think they have the appropriate level of expertise.”

It’s all about access

Access to the crème de la crème of alternative managers challenges most tax-exempt institutions and family offices, but OCIOs, with the diversified endowment model as their template, have spent years sourcing and cementing relationships with top private equity and venture capital professionals. Providers now offer a variety of alternative sleeves for those who prefer specialized participation.

A few prescient firms have gotten even more creative. McMorgan & Company, for example, has an infrastructure fund not common in boutique outsourcers.

A few years ago, the company established a relationship with OMERS Infrastructure, the infrastructure investment arm of OMERS, a large Canadian pension plan that has been investing directly in infrastructure since 1999. This relationship has led McMorgan to create a fund which co-invests in certain deals alongside OMERS Infrastructure.

There’s nothing new about infrastructure funds, plenty of firms in the mix, but few boutiques take the time to build something special. The McMorgan Infrastructure Fund hews a path for prudent tax-exempt and family office investors.

Final thoughts

We’re in the executive search business, for those that haven’t already guessed, along with OCIO search and selection and the occasional consulting assignment, so job seekers send us resumes and call almost every day.

Most candidates hammer on about what they’ve got and what they want. Surprisingly few spend much time asking about what our clients want, the folks we care most about.

But now and then someone applies that “second level thinking” Howard Marks talks about. They surprise us by connecting the dots, by carefully researching a potential employer and asking, what does this company need and how can I give it to them, rather than ramble on about what they, the job seeker, wants.

Here’s an example, a story we heard some while back.

Read More »OCIOs: the price of impatience

by charles | Comments are closed09/18/2024

“The thing that never happens just happened again” – Viktor Chernomyrdin, former Prime Minister of Russia

Our latest Outsourced Chief Investment Officer spot-check notes a steady stream of RFPs, mostly under eighty million AUM, Obama Foundation excepted.

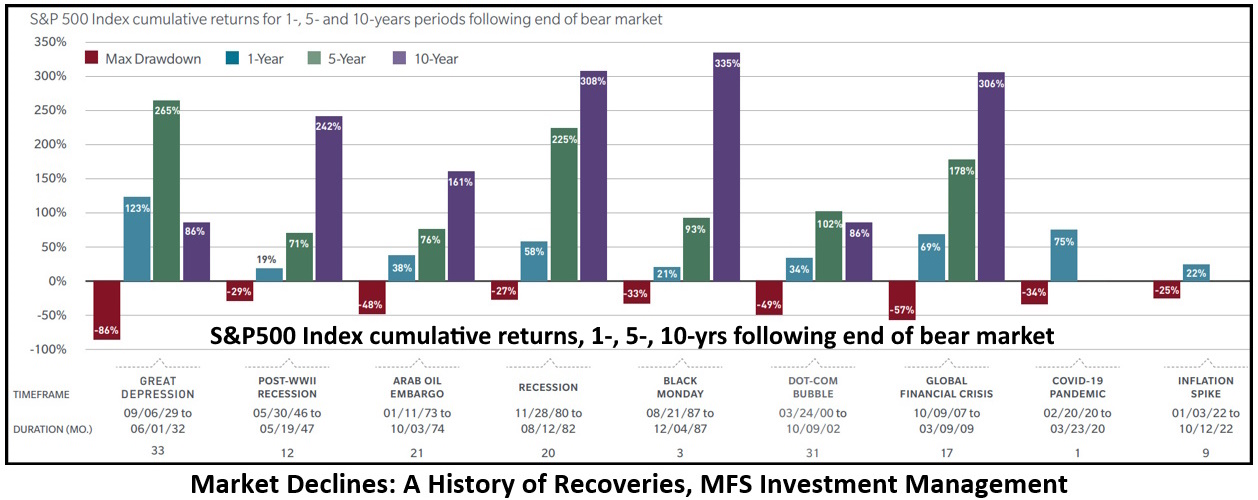

Some client institutions are looking to change providers, unhappy with recent returns. But if better performance is what they’re after, a word of caution: their current OCIO’s best years might be just beginning.

Even Berkshire Hathaway, with one of the best runs ever, “has had 10 negative return years, four years where it has fallen greater than -20% and six years where it underperformed the S&P500 by more than -20%.”

Apples and oranges

How should one compare OCIO returns? Commonfund considers comparisons “a complex apples-to-oranges exercise because there are so many variables to consider. Performance outcomes are as unique as the institutions themselves.”

We keep track of over one hundred OCIOs. Each has its own culture, client mix, investment style, and biases. Some firms focus on indexing and liquid markets, others on alternatives, still others on ESG. Some customize portfolios for clients, others don’t.

When we speak of past performance we are referring to history. But forecasting what’s to come is mostly an expression of hope. And hope is not a strategy, or reason to change providers.

According to Business Insider, “the S&P 500 average return over the past decade has come in at around 10.2%, just under the long-term historic average of 10.7%.”

Does this mean all OCIOs or clients should have indexed and gone home? Are they sure these public market returns are baked in for the next ten to twenty years? As Brad Conger at Hirtle Callaghan wrote a while back, “not even the most insightful among us can see around corners.”

“Historically, markets have posted strong long-term gains following declines,” but that’s over ten years and more. For most investors, or board members, patience is not their strong suit. Unfortunately, there’s usually a price to pay for impatience.

{kind=link}

People come first

We begin an OCIO search and selection assignment by looking at the talent. Who are they, what is the turnover, how long has the firm been in business, and what’s their plan for staying on top? Then investment philosophy, process, and incentives. Then performance.

In the end it’s the ability to adapt, revitalize, and deliver over time that’s key. Brown Brothers Harriman, Goldman Sachs, J.P. Morgan, and Morgan Stanley have been around for more than a century and they keep signing up clients.

But how about the eighty or so OCIO firms in our last directory under fifty billion AUM? Hirtle Callaghan, Commonfund, and a few others have engineered smooth successions. Yet most still have first-gen founders in place or soon to retire. What comes next?

There’s a related issue. What happens when outside money enters the picture? Will the passion and focus remain? Or will the firm lose the founder’s intensity and become one more commodity in a collection of disposables?

Final thoughts

As we’ve said many times before, given the talent and resources in this country, the chances of building top-ranked, enduring investment teams capable of vaulting over the competition are slim to none without superior technology, blockbuster products, or a relentless M&A machine.

If the goal is to deliver exceptional performance, service and solutions and be there for the client over decades, forget about reinventing the wheel. Talk to your competitors. Some might make fine partners.

———————————————–

Time to update our OCIO directory

It’s time once again to update Skorina’s Outsourced Chief Investment Officer (OCIO) directory. So please send us any changes in contact information (name, phone, email) and AUM as of June 30, 2024.

Prospective clients can’t reach you if they don’t know how to find you.

—Charles Skorina

Read More »Why take a chance?

by charles | Comments are closed08/13/2024

“If I had asked my customers what they wanted they would have said a faster horse.” —Henry Ford

If you were sitting on a college board today, would you take a chance and hire a young David Swensen or Paula Volent to manage the money? Radical thinkers cut from uncommon cloth?

Let’s reframe the question. If institutional investing is all about finding alpha and maintaining an edge, why are so many tax-exempt institutions investing and hiring alike?

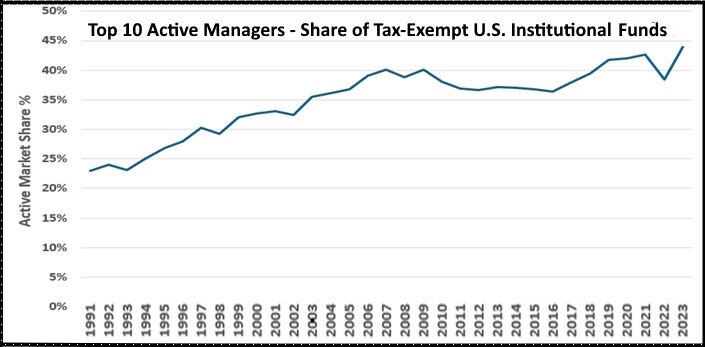

Almost forty-five percent of U.S. tax-exempt money is invested with just ten active managers, nearly double the amount two decades ago. To quote one reader’s response to our recent query, “everyone’s in the same funds and there’s leverage everywhere.”

(click link for chart. Data from P&I, chart by Robert Snigaroff, President & CIO, Denali Advisors)

{kind=link}

In theory, pensions, endowments, foundations, and the like seek active managers to obtain above-market returns. In practice, that doesn’t seem to be how it works.

A former large endowment CIO mentioned recently that his team would scour the globe for unique opportunities, but the first thing his trustees would ask when told of any rare find was “what other endowments have invested in this?”

Safety in numbers

Most trustees accept the position because they love their institution, and often pay for the privilege, but the reputational risks of sitting on a nonprofit board outweigh the rewards. Media assassinations felled some well-meaning board members recently.

Let’s be honest. If the David Swenson of 1985 applied for a CIO position at Yale today, he would not survive the first round of interviews — a young untested Wall Street banker, working on something called interest rate swaps? No way.

And how about Paula Volent, for twenty years the preeminent CIO at Bowdoin College, currently at Rockefeller University? Year after year she has crushed our endowment rankings.

But she was an art history major running a West Coast fine arts conservation business before her swing to a Yale MBA and money management. Would any college board dare hire someone with that background and mid-career makeover today?

The horns of our dilemma

Here’s our challenge. If boards want a “faster horse” they may not appreciate being shown EVs.

Our pool of investment talent includes hundreds of tax-exempt endowments, foundations, public and private pensions, health systems, associations, and charities, and thousands of for-profit analysts and managers at funds, family offices, OCIOs, RIAs, Wall Street banks, and asset managers.

Yet roughly sixty-five percent of endowment hires come from other endowments, a safe and like-minded cadre of about a hundred candidates.

But that’s not the only bottleneck. In the E&F world, men are twice as likely to land a chief investment officer position as women despite a near fifty-fifty split in staff roles. Our women in finance report focused on the time it took the double X cohort to reach CIO positions.

We counted heads and reviewed backgrounds and what did we find? Most female chief investment officers had an additional five to ten years of work history on their resumes compared to the men. In other words, the men were younger than the women when hired for CIO roles – ten years on average – with less experience.

And forget that hackneyed trope about taking a break for babies. Most served hard time at Morgan Stanley, Montgomery Securities, Goldman Sachs, and other financial firms while raising a family.

The gist is that board members seem more inclined to take a chance on younger men than younger women, which leaves fifty percent of the talent pool out to dry. We who recruit investment talent for industry-leading firms, funds, and families have learned that gender has no bearing on investment performance.

Words worth repeating

For those of us that hunt talent for a living, character, compatibility, and content are key. Character embodies the qualities that define the individual, compatibility – that elusive emotional IQ that Daniel Goldman writes about – builds trust, and content is knowledge and experience accumulated over a lifetime.

Read More »Anything new under the sun?

by charles | Comments are closed07/27/2024

“There’s only one way to describe most investors: trend followers.” —Howard Marks

We recently sent out an email query asking asset managers and chief investment officers, “anything new under the sun,” and received some serious replies. One thoughtful, highly respected, mega-fund chief investment officer wrote:

“There are quite a few interesting trends: AI, energy transition, innovations in healthcare are a few positive ones. Commercial RE, small cap, China and Emerging Markets are a few negative ones.

“The slow pace of private capital coming back to investors is another important trend that everyone is contemplating. Everyone is hoping that lower interest rates will restart more M&A and IPO activity.

“However, personally I think the bigger trend is how investors are thinking about asset allocation. I remember the strong emphasis across the industry on diversification. If you could find uncorrelated return streams, the trend was to add them almost blindly. Diversification and low vol was the main point.

“Today (and for some time), diversification has not been your friend. The future is moving to disruption, and you need companies and funds that have size, data, the ability to invest in AI, and cheap financing.

“Disruption is so large in the U.S. that we may not need geographic diversification like we used to.”

Another CIO replied:

“I find the dominance of U.S. public equities, and a teeny-weeny handful of them at that, to be quite troubling.

“One of our IC members is pushing us to divest of non-U.S. equities and it’s difficult to find any recent data to argue against that, yet the idea of having 40% of our endowment in a stock portfolio that’s really just five giant tech stocks is scary to me.

“We’ve reduced our hedge fund exposure, our real asset portfolio was always pretty small, and those big tech companies are amazing economic engines, so I am not sure I would say we are in a bubble.

“But some of the most successful endowments have one-sixth, one-fifth, or even one-quarter of their portfolios with a single VC firm. Maybe we should be worried.”

Pay and Chief Investment Officers

Speaking of chief investment officers, in case you missed it, here are a few highlights from an interesting paper on chief investment officer compensation by Matteo Binfarè, University of Missouri and Robert S. Harris, University of Virginia:

“Endowments pay CIOs more, rely more on bonuses, attract more experienced professionals, and have lower turnover than pensions.

“On average, endowment CIOs earn a whopping $800,000 in total annual compensation, three times more than their peers at pension funds. Incentive compensation makes up a significant portion of their pay, with more than 40% being tied to incentives — almost four times more than pension plan CIOs.

“Endowments that pay their CIOs top quartile compensation significantly outperform endowments with bottom quartile compensation by almost 100 basis points annually.”

All great stuff, but this begs the question, what are chief investment officers actually getting paid for? Size, complexity, performance?

The compensation conundrum

According to Business Insider, “the S&P 500 average return over the past decade has come in at around 10.2%, just under the long-term historic average of 10.7% since the benchmark index was introduced 65 years ago.”

Read More »Affluent Family Affairs

by charles | Comments are closed07/22/2024

Money, if it does not bring you happiness, will at least help you be miserable in comfort. —Helen Gurley Brown

While family dynamics probably haven’t changed much since Count Leo Nikolaevich Tolstoy wrote his famous line about unhappy families, the modern family office has come a long way from 1878 when Anna Karenina was published, adding structure, discipline, academic rigor, and, most importantly, convenience to the management of UHNW affairs.

Ultras place a premium on convenience and they are more than willing to pay for it. Whether it’s a dedicated family office or a cadre of wealth and client service providers, when you’ve made it big, you need a lot of help, as Deloitte explains in a recent report. There are operating companies and investment portfolios, estates and staff, trusts, foundations, donor-advised funds, art collections, cars, boats, and planes, accountants, lawyers, and specialized service providers.

Here to help

We’ve been sifting through this rarefied mix of New York wealth and family service elites, on assignment for a notable Wall Street firm. Our mandate? Recruit a professional client service maven who will make the partners’ lives easier and their balance sheets stronger.

Firms like Goldman Sachs, KKR, and McKinsey have dedicated concierge groups to service their partners. Goldman, in fact, just renamed their partners coverage group the “partners family office.”

One candidate with considerable experience working for billionaires described the work this way:

“My writ was straightforward, Charles: create wealth, reduce taxes, and mitigate risk. But the job was a little more complicated than that.

“Over the years, I’ve worked with experts on investments and allocations, restructured lines of credit, and arranged and refinanced mortgages. I dealt with accountants, attorneys, and realtors, bought and sold property, art, and collectibles, researched state and global tax domiciles, and negotiated loans on assets. Whatever the client wanted, you name it.

“But in this job you also have to read people and be the consummate diplomat. As families grow larger and wives and husbands come and go, competition increases for access and influence. Don’t ever forget who you work for.”

Where are the ultras?

It’s tough to get a handle on the number of ultra-high-net-worth families in the US, the assets they control, or their objectives because most prefer the shadows to the limelight.

In one widely quoted survey, Campden Wealth reckoned there were 3,100 large single-family offices in North America. The Family Office Exchange (FOX), on the other hand, cast a wider net, estimating closer to 10,000 SFOs given the relentless growth in global wealth.

As for billionaires, the Hurun Global Rich List 2024 counts one-hundred-nineteen billionaires in New York while Henley Global’s World’s Wealthiest Cities Report 2024 uncovered a mere sixty.

Chart: US cities with millionaires, centi-millionaires, billionaires

As an aside, of the roughly $83 trillion in wealth transfer over the next twenty years, according to the UBS Global Wealth Report 2024, “a notable amount of this wealth will move horizontally between spouses first, before moving to the next generation. In practice, this means a considerable transfer of wealth to women, considering their comparatively higher life expectancy.”

What’s a client service professional?

Read More »{kind=link}