Endowment Performance 2024: How Sweet It Is

by charles | Comments are closed01/18/2025

Being too far ahead of your time is indistinguishable from being wrong — Howard Marks

Our latest fiscal year-end 2024 endowment performance report features ten-year and one-year returns, and AUM for one-hundred-forty-four US and eight Canadian institutions, the latest available.

In our line of work, acquiring talent and capabilities for institutional and family office clients, we like hard data on the individuals who drive the investment decisions. Returns may be historical, but they are useful clues to an investor’s – and board’s – views, process, and discipline.

We consider a ten-year span to be a rigorous and revealing measure of the strength of an institution’s long-term investment abilities, but we remind our readers that there’s much more to the story.

Board members and administrators set the parameters for investment execution, and they are the ones to judge whether their goals are met. Every school has its own endowment payout rate and tolerance for risk and that’s what CIOs aim for. Some schools rely heavily on income, others place more weight on growing the principal.

A tale of two markets

For those institutions holding substantial U.S. public equity stakes life is sweet. As Chris Markoch at MarketBeat writes, the S&P was up twenty-three percent in 2024, “driven by earnings growth and sector leaders in AI, biopharma, and blue-chip companies.”

Sometimes it’s best to run with the herd, to paraphrase our Mr. Marks. But for endowments with heavy exposure to alts, particularly private equity, there were challenges.

PE has performed well for forty years. But there are periods when the economy tanks, deals stagnate, and returns to investors slow to a trickle.

Here’s Peter Lynch’s droll take on fickle Mr. Market, and a few partisan comments on PE from Alisa Amarosa Wood and Chris Harrington, partners at KKR, and Ludovic Phalippou, professor of Financial Economics at Saïd Business School, University of Oxford.

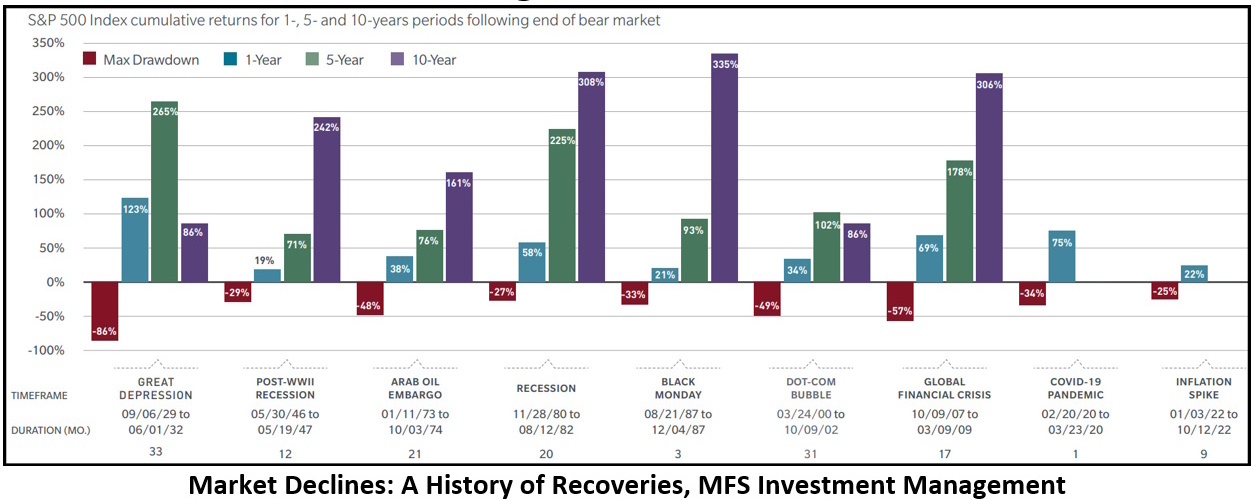

Opposing pundits aside, we take comfort in the chart below, a cheerful visual we ran in September’s newsletter from MFS investment Management depicting the S&P’s bumps and grinds.

S&P 500 Index cumulative returns for 1-, 5-, and 10-year periods following end of bear market

{kind=link}

Tenure and Turnover

What a difference a decade makes. Only about a third of the CIOs in our FY2024 endowment investment report logged ten years or more tenure, and those are mostly the ones on top.

Mr. Philip Zecher, CIO at Michigan State University, and our featured guest below, will soon pass the ten year mark and the endowment’s splendid performance reflects his time and attention.

Chief investment officers new to the position, Ms. Geeta Kapadia at Fordham for example, barely have time to roll up their sleeves and grab a pitchfork. It takes five years at least to clear, plough, and seed an endowment, and five more to fully bear fruit.

College endowments consist of thousands of gifts with strings and legally binding contracts attached. To repeat a well-worn trope, it takes years to fully implement a multi-asset, multi-generational investment strategy and altering course mid-stream – a new investment chair, a change in CIOs, court battles – can sap performance for a decade.

————————————————–

Phil Zecher, chief investment officer

Michigan State University

Read More »{kind=link}